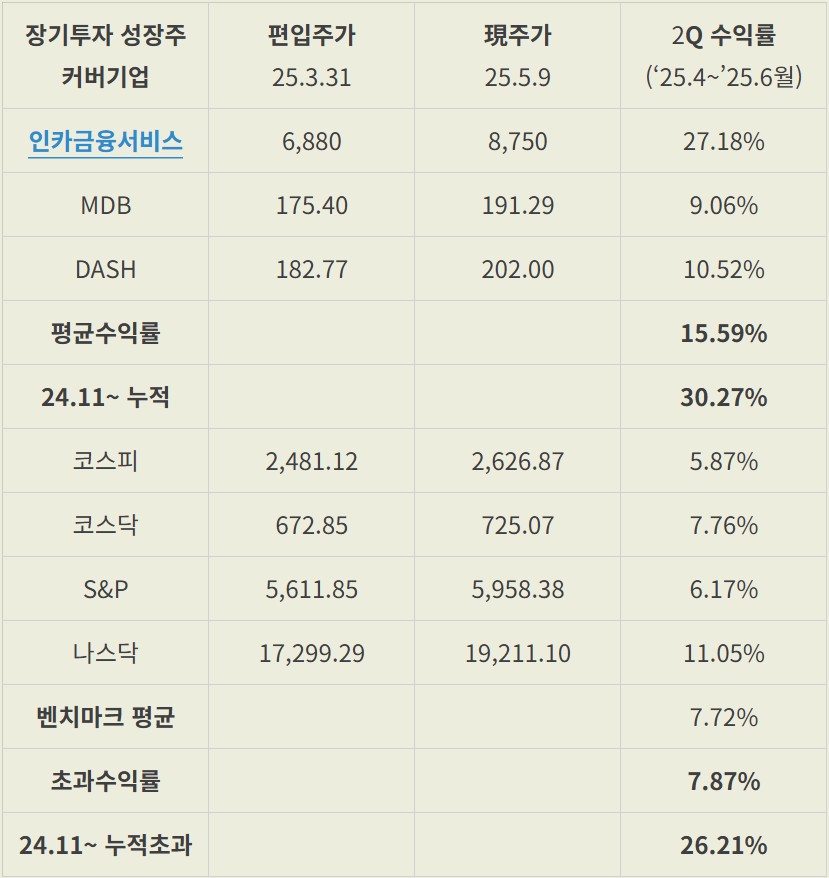

‘25.5월 셋째주는 전체적으로 시장이 회복세를 보이면서 커버기업들도 주가가 회복세를 보였다.

이런 시기일수록 수익률을 차별화하기가 쉽지 않은데, 국장이 다소 지지부진한 가운데 미국 주식이 힘을 내줘서 시장 대비 아웃퍼폼하면서 초과수익률이 꽤 올라왔다.

인카금융서비스는 순항하고 있으며, DASH도 매출 2% 미스가 큰 성장 추세에서 의미를 두기 어렵다는 것을 시장이 충분히 인식한 것으로 생각된다. MDB는 6.4일 실적 발표를 앞두고 있다.

https://cafe.naver.com/ltoptimization/464 RELY는 임원 매도 뉴스로 주가가 내려왔다. 사실 RELY가 무슨 신약 임상중인 기업도 아니고 임원이 시장참여자에 비해 얼마나 많은 정보를 가지고 있다고 한 20억원 어치 주식 매도한 걸로 주가가 내리는 건지 잘 이해는 가지 않는다.

그리고 불법 이민자들 송금에 5% 세금을 매기는 법안이 발의된다고 하는데, 디지털 송금시 비지디털 송금에 비해 인적 검증 절차가 훨씬 간편하기 때문에 오히려 경쟁력이 올라가는 이벤트이다.

주가가 내려갈수록 더 싸게 살 수 있음에 감사할 수 있는 주식만으로 포트폴리오를 채워나가는 것이 가치투자자의 책임이 아닐까?

인간은 실수를 할 수 있지만 로봇은 실수를 하지 않으며, 섬세함과 정확성을 극한으로 끌어올릴 수 있어 선호도가 높아지고 있다.

또한, 절개 면적을 분산, 극소화하여 수술하는 등 수동으로는 불가능한 창의적 방식의 수술이 가능해지면서 로봇 수술이 굉장히 각광받게 될 것으로 예상된다.

이 분야에서 가장 선두에 서 있는 Intuitive Surgical은 당연하게도 상당한 멀티플 프리미엄을 받고 있다.

하지만 매출의 성장률은 아직도 충분히 가파르며, 타겟 시장은 수술이 필요한 광범위한 의료 수술 시장으로 잡을 수 있기 때문에 아직도 갈 길이 멀지 않을까 생각된다. (리포트에 따르면 아직 전세계적으로 만 대 내외밖에 판매되지 않았다고 한다. OECD 평균 1,000명당 의사수는 3.7명, 인구수는 13억명이므로 의사 수는 481만명이다) 의사들의 수술을 100% 대체한다고 가정하면 앞으로 갈 길이 한참 남았지 않았을까?

물론, 리포트에서도 말하듯이 J&J, 메드트로닉, 뉴럴링크 등 다수의 기업들이 로봇 수술 시장 진입을 노리고 있다.

TSMC는 관세 인상 전에 칩 재고를 축적하려는 수요 때문에 4월 사상 최대 매출을 달성했다고 한다. 하드웨어 투자가 계속 이어져야 한다고 하면 최대 수혜주라는 데에는 의심할 여지가 없다. 다만, 현재 내 생각으로는 소프트웨어 기업들쪽으로 더 시장의 선호, 궁극적으로는 돈의 흐름이 이어지지 않을까 싶다.

담배를 피워본 적이 없어서 잘 모르지만, ‘담배 끊은 사람은 상종도 하지 말라’ 는 말은 들어본 적 있다.

그만큼 금연이 힘들다는 뜻이니까 이를 BM으로 하는 회사는 해자가 굳건하지 않을까 생각이 되기도 한다.

K-담배의 경쟁력이 무엇인지 이해가 가능하다면 투자가 가능하지 않을까?

가치투자 커뮤니티를 성장시켜나가고 있습니다. 운영 계획과 방향성을 한 번 읽어보시고, 텔레그램과 유튜브 채널을 통해 소통하고 있으니 공감이 가신다면 참여해주세요! 쌍방향 소통을 원하는 분들은 카카오톡 채널로 와 주시면 좋을 거 같습니다. 자료실을 통해 리포트, 뉴스도 공유하고 있으니 참고하시면 도움이 될 거 같습니다.

’24년 당기순이익은 $1.23억, 현재 시총은 $810억으로, ’24년 TTM PER은 658.5이다.

또한, 시총 $810억은 한화 119.1조에 달하며, 이는 코스피 시총 3위에 해당하며, 현대차-기아를 합산한 시총보다 비싸다.

많은 사람들은 이런 밸류에이션이 터무니없이 비싸다고 할 수 있을 것 같다.

하지만 나는 ‘글로벌 통합 로컬 커머스 기업’으로서 DASH가 추구하는 거대한 스케일의 비전이 달성될 가능성이 매우 높고, 비전이 실현된 시점의 기업가치는 현재보다 몇 배는 더 높게 평가되어야 한다고 생각한다.

이러한 평가의 근거는 강한 경제적 해자, 협상력을 바탕으로 한 앞으로의 이익 성장, 성장하는 시장 속에서도 적재적소에 투자를 통한 경쟁사 점유율 침식 등이다.

이러한 판단의 근거를 구체적으로 정리해보고, 더 많은 사람들의 피드백을 통해 투자 아이디어를 더욱 정교하게 발전시키고 싶다.

DASH의 BM

BM의 구조

DASH는 기본적으로 우리 나라의 배민, 쿠팡이츠와 같이 ‘음식 배달업’을 한다.

배달 플랫폼에서 소비자가 음식을 구매할 때 발생하는 매출은 크게 네 가지이다. 1. 소비자가 내는 배달비 2. 소비자가 $12 이상 주문시 배달료를 면제받는 DashPass에 가입하면 받는 월회비($9.99/월) 3. 입점 상인이 내는 수수료(take rate : GOV, Gross Order Value, 총 주문액의 일정 비율) 4. 소비자 트래픽에 따라 입점 상인 광고, 상위노출 등에 대해 받는 광고료

그리고 사업을 하면서 발생하는 주요 영업비용은 다음과 같다. 1. 배달기사(Dasher)에게 지급되는 배달료 2. 플랫폼 구축(카테고리/지역 확장시), 운영(업데이트) 비용 3. 기술개발(R&D) 4. 광고료

DASH는 미국 음식점 배달 시장에서 확보한 소비자 트래픽을 바탕으로 로컬 유통 플랫폼을 식료품, 편의점, 리테일, 주류, 공구, 스포츠용품, 사무용품, 반려동물, 헬스, 화장품 등 다른 상품 카테고리로도 확장해나가고 있다. (식료품의 경우 20년 하반기 코로나 시기 서비스 시작하여 23.3Q 기준 10만개 이상 비음식 상점이 플랫폼에서 상품/서비스 제공중, 신규 고객 중 절반이 비 음식 카테고리로 앱에 방문) 이런 카테고리 확장은 네트워크 효과를 더 강화해주는데, 이에 대해서는 경제적 해자에서 자세히 설명하겠다.

또한, 지역적 측면에서도 캐나다, 호주 등 30개국으로 확장해나가고 있다. 이러한 지역적 확장시 DASH의 강점에 대해서도 경제적 해자에서 자세히 설명하도록 하겠다.

DashPass 구독 매출의 수익성 기여

다른 매출의 경우 늘어날수록 수익성에 기여하는 것이 직관적이다. 하지만 구독은 늘수록 배달료가 면제되기 때문에 수익성이 악화되지 않나 의문이 생긴다.

우선, 구독한 소비자는 매월 $9.99를 지불하기 때문에 DASH 매출의 변동성이 완화된다. 또한 구독료 매출은 증가하는데 비용이 들지 않기 때문에 수익률을 높여준다.

그리고 구독을 하게 되면 소비자 입장에서는 배달 횟수, 배달 크기(Order Value)가 증가하더라도 추가 비용이 없기 때문에 자연스럽게 이용을 늘리게 된다.

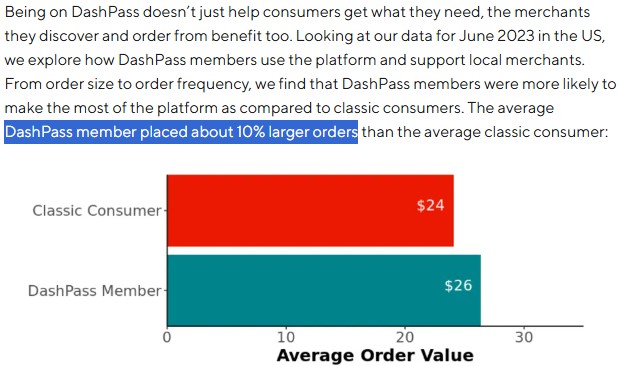

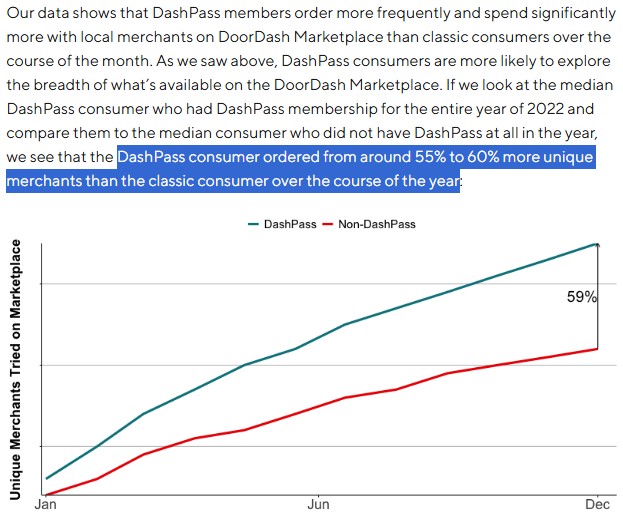

아래 표는 DashPass 이용자의 평균 주문 금액이 10% 더 많다는 내용이다.

또한 DashPass 이용자는 59% 더 다양한 음식점/식료품점을 사용한다는 통계이다.

이러한 사용량 증가에 따라 결국 입점 상인이 DASH에 내는 수수료가 증가하게 된다.

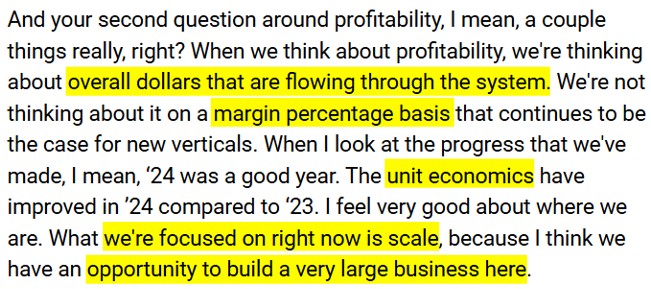

특히 구독자수가 증가하여 배달료 면제 비율이 높아지고 있는 가운데, ‘24.4Q 컨콜에서는 각각의 거래가 모든 변동비를 제외하고도 수익성을 달성하는 단위 경제성(unit economics) 측면에서 수익을 달성하고 있음을 밝히고, 따라서 앞으로 중요한 것은 수익성 확보보다 규모를 확장하는 것임을 강조했다. (거래량만 늘려나가면 이익은 따라온다는 의미)

또한, 사용량이 증가하면 단위 배달비용도 절감되는 ‘규모의 경제’효과를 누릴 수 있다. 이에 대해서는 경제적 해자의 근거로서 규모의 경제에 대해 논의할 때 설명하겠다.

결과적으로 DashPass를 통해 잠재 소비자 규모와 그들이 주문량을 확대시켜 플랫폼으로부터 소비자와 배달원, 상인 모두가 얻는 것을 극대화하는 구조를 만들고, 이에 따라 플랫폼이 선순환을 이루면서 충분히 커질 때까지 성장하는 ‘큰 시장 내러티브’를 구상하고 있는 것이다.

광고

DoorDash는 음식점, 브랜드 뿐만 아니라 일반 소비재 기업들의 광고까지도 게시하여 수익성 높은 매출을 얻고 있다.

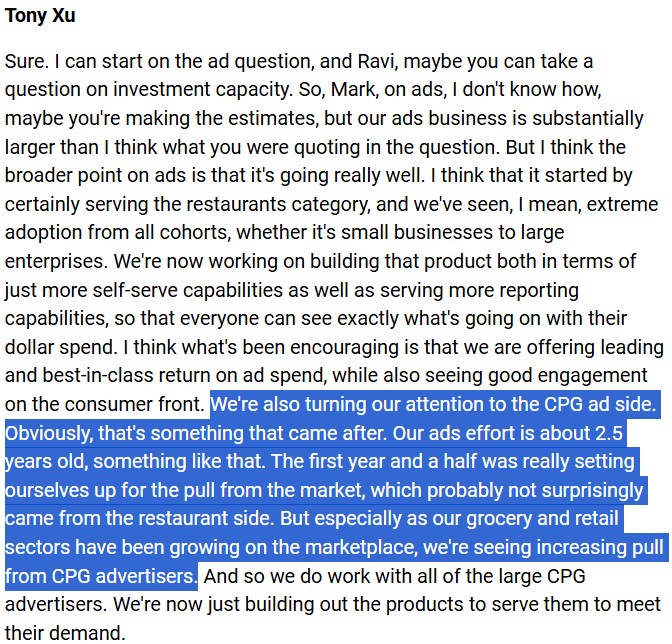

‘24.1Q 컨콜에 따르면 ’21년 말부터 광고 사업이 시작되어 ’24년부터는 소비재(CPG) 광고주로 광고 대상이 확장되고 있어 수익성에 긍정적인 기여를 하고 있다.

특히 배달 앱을 사용하고 DashPass까지 사용하는 소비자라면 구매력이 확보되기 때문에 매력적인 소비자가 많은 온라인 광고 채널이라는 점에서 향후 매출 성장과 수익성 개선 측면에서 큰 기여가 기대된다.

Logistics & 3P(third-party)

DASH는 상점들이 자체 웹사이트/앱을 통해 주문을 받고 그때그때 DASH에 유통을 의뢰하는 On-Demand 배달 솔루션인 DoorDash Drive 서비스나, 독자적인 판매 채널을 만드는 것도 지원(DoorDash Storefront)하고 있다.

이를 통해 상인들은 DASH의 강한 유통망을 활용할 수 있게 되며, DASH 입장에서는 규모의 경제를 확대시키는데 기여하게 된다.

It’s the logistics, stupid

클린턴 대통령이 1992년 대선에서 부시 전 대통령을 이기고 당선된 주요 이유 중 하나로 ‘중요한 건 경제’라는 구호를 이야기하는 사람들이 많다. 92년 대선 이후 중요한 게 뭔지 잊어버린 사람들에게 정말 중요한 걸 알려주는 일종의 밈으로 It’s the ____, stupid가 사용되어 왔다.

이 오래된 밈을 사용할 때가 왔다. It’s the logistics, stupid.

국장에서도 그렇지만 미장에서도 어이없는 기사가 나올 때가 있다.

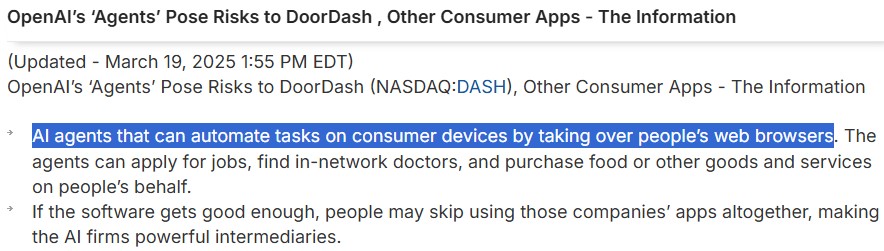

AI 에이전트가 주문을 자동화하여 DASH의 사업이 침식될 수 있다는 주장이다. 나는 이 기사를 작성한 기자가 DASH의 사업을 제대로 이해하지 못했다고 생각한다.

AI가 식당에 주문을 넣고 정산하는 것까지는 자동화할 수 있을 것이다. 하지만 이 영역은 해자가 강한 영역이 아니어서 경쟁사가 쉽게 모방할 수 있으며, 따라서 DASH의 사업에서도 중요한 부분이 아니다.

하지만 AI 에이전트가 식당에서 소비자에게 저렴한 수수료만 받고 신속히 배달해줄 Dasher를 찾아서 소비자의 손에 따뜻한 음식을 전달해주는 것을 자동화할 수 있을까?

결국, DASH의 사업은 본질적으로 ‘유통 플랫폼’이다. 좀 더 구체적으로는 Last-Mile-Delivery, 즉 배송의 가장 마지막에서 실제 소비자에게 상품(음식)을 전달해주는 BM이다. 이 BM은 구조화, 정량화, 정형화가 극도로 어려워 자동화가 가장 더딘 영역이다.

DASH의 성장성

타겟 시장

DASH의 상위 시장은 유통 플랫폼으로, 아마존, 알리바바, 쿠팡 등 전자상거래 기업들이 모두 포함된다. 조금 구체적으로는 로컬 커머스를 기반으로 한 Last-mile-delivery를 타겟 시장으로 한다. 이 시장에는 Uber Eats, Deliveroo 등 기업이 포함되나, 이들 기업보다 훨씬 더 큰 내러티브를 추구한다.

지역적으로는 미국 시장을 기반으로 캐나다, 유럽, 호주, 일본 등 국가에 진출하여 빠르게 사용자와 매출을 성장시켜나가고 있다.

카테고리 측면에서는 음식 배달을 기반으로 식료품, 편의점, 공구, 주류 등 다양한 카테고리의 로컬 커머스 시장으로 확장을 추구하고 있다.

온라인 배달 시장의 성장성

DoorDash는 음식점 배달 플랫폼으로 시작하여 아직도 꾸준히 성장하고 있지만, 더 큰 성장을 위해 식료품, 편의점, 리테일 등 카테고리 확장, 캐나다, 호주, 유럽 등 아직 침투율이 낮은 국가로의 지역적 확장을 통해 성장 내러티브를 더 크게 확장해나가고 있다.

쿠팡이츠, 배민을 써본 사람이라면 모두가 공감할 것이다.

한 번도 안 써본 사람은 있어도 한 번만 써본 사람은 없다.

이러한 소비자 편의성은 온라인 배달 시장이 성장할 수밖에 없는 근거가 된다.

음식 시장의 성장과 온라인 배달 시장 침투율

미국 온라인 음식 배달 시장 침투율

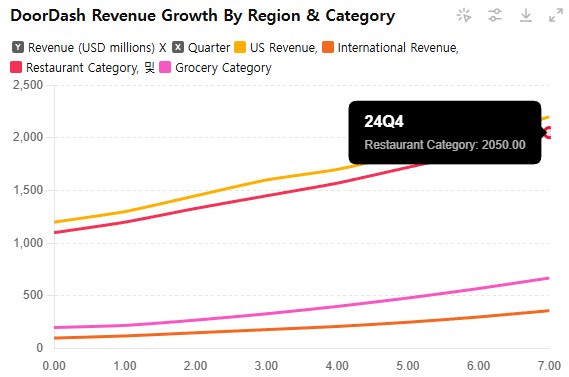

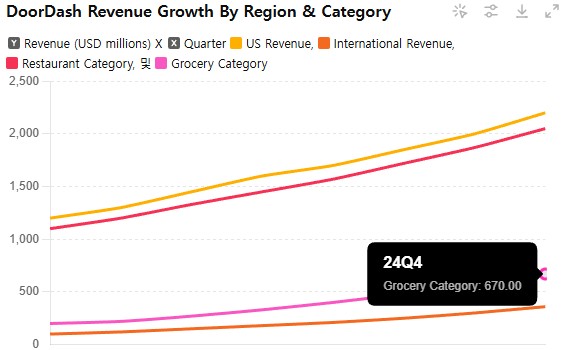

미국 시장에서 DoorDash의 점유율이 67%이며, ‘24.4Q 총매출 $28.7억에서 수출은 $3.6억, 미국 내수는 $25.1억로 비중은 87.5%이다. 그리고 식료품 배달 매출은 $6.7억, 음식 배달 매출은 $20.5억로 비중은 71.4%이다. 따라서 DASH의 미국 음식배달 매출 비중은 62.5%이고, ’24년 총 DASH GOV가 $802억이므로 미국 내수 GOV는 $501.3억이다. 따라서 전체 온라인 음식 배달 시장 규모는 501.3/0.67=$748.2억이다.

따라서 온라인 음식 배달 시장 침투율은 7.5%로 한자릿수 수준으로 파악된다. 이는 아래 24.4Q 컨콜을 비롯하여 여러 번 컨콜에서 언급된 ‘한자릿수 침투율’과 일치하는 추정 결과이다.

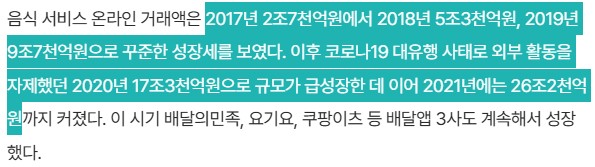

한국 온라인 음식 배달 시장 침투율

그렇다면 어디까지 침투율이 올라갈 수 있을까?

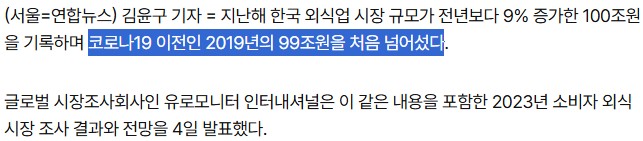

한국은 인구밀도, 도시화율 측면에서 미국에 비해 온라인 음식 배달에 유리한 상황으로, 배민, 쿠팡이츠 등 가장 온라인 음식 배달 시장 침투율이 높은 국가 중 하나이다. 그럼에도 불구하고 앞으로 미국, 다른 국가의 배달 시장 침투율 향상 여력을 검토하는 차원에서 한국 시장에서 온라인 음식 배달 시장 침투율을 알아보겠다.

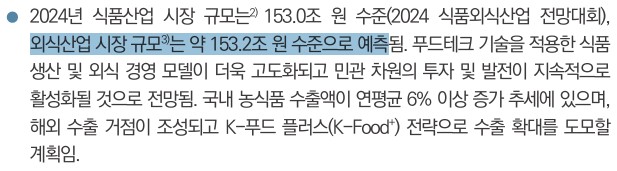

‘24.3Q 누적 온라인 음식 배달 거래액은 21.4조원이며, 연간 거래액 추정치는 28조원이다. 그리고 농경연에 따르면 ’24년 외식산업 시장 규모는 153.2조원이다. 따라서 ’24년 온라인 음식 배달 시장 침투율은 18.3% 수준으로 추정된다.

따라서 ’19년 온라인 배달 침투율은 9.8%이다. ’20년 코로나가 있었지만, 5년만에 침투율이 9.8%에서 18.3%로 8.5%p 증가하였으며, 이런 사례로 보아 미국 시장도 앞으로 갈 길이 상당히 남았다는 추정을 가능하게 해준다.

식료품 온라인 배달 시장 침투율

마찬가지로 식료품 배달시 이용 경험에 대한 만족도 확보, 이에 따른 평균 배달액 증가와 이용자수 증가로 식료품 배달 침투율이 급상승하고 있다.

나도 식자재는 직접 마트나 시장에 가서 보고 사야 한다는 인식이 있었는데, 최근 쿠팡, 홈플러스, 이마트 등 인터넷 쇼핑은 질낮은 상품을 제공하면 경쟁에서 뒤쳐지기 때문에 ‘전문 픽커’가 고품질 상품을 선별해서 제공하고, 어떨 때는 내가 마트에서 고른 것보다 더 신선하고 맛있는 제품이 온다고 느낄 때도 있다.

아쉽게도 식료품 배달은 시장 점유율 정보가 없어 침투율 추정이 어렵지만 현재는 선도 기업인 Instacart의 점유율이 50% 이상으로 추정된다.

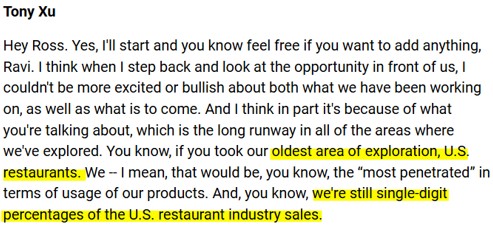

하지만 23.1Q 컨콜에서 Tony Xu가 식료품 배달 시장 침투율이 레스토랑 배달 시장에 비해 몇 배 낮은 수준이라고 언급하여 미국 식료품 배달 시장은 상당히 초기 단계임을 알 수 있다. 따라서 쿠팡이 쿠팡이츠로 성공적으로 확장한 것과 반대로 DASH는 음식 배달 시장의 압도적 점유율과 트래픽, DashPass를 바탕으로 식료품 시장으로 성공적으로 카테고리 확장을 하고 있다. (24.3Q $5.7억, 23.4Q $3.3억 vs. 24.4Q $6.7억, QoQ 17.5%, YoY 103.0%)

DASH의 경제적 해자

브랜드가치

더 빠르게, 보다 소비자 선호에 부합하는 음식/상품을 제공함으로써 DoorDash의 음식/상품에 대한 브랜드가치가 높아진다.

전환비용

소비자

소비자들은 DashPass에 가입만 하면 음식 배달 뿐만 아니라 다양한 상품을 구매하는 편의성이 전반적으로 개선되기 때문에 쉽게 가입을 탈퇴하지 못한다.

특히 원래 음식을 배달시켜 먹던 소비자 입장에서는 별도 카테고리가 들어옴으로써 Pass 가입의 효용이 더 높아지게 되면서 DashPass 탈퇴에 따른 비용이 더 커지게 된다.

상인

상인 입장에서는 사업장을 확장하지 않고도 용이하게 추가 소득을 발생시킬 수 있는 매출원이 되므로, 다수의 플랫폼간 경쟁 구도가 유지되어 낮은 수수료율이 유지되는 것이 바람직하다.

하지만 소비자는 하나의 Pass 가입으로 더 큰 혜택과 낮은 배달비용으로 다양한 쇼핑을 할 수 있는 DASH 앱으로 몰리게 될 가능성이 높으며, 결국 소비자가 늘어나는 쪽이 더 수수료율이 높더라도 입점하여 서비스를 제공하는 것이 유리하다.

또한, 한 번 입점하게 되면 시장의 지배적인 플랫폼을 통한 주문 비중이 높기 때문에 이로부터 이탈하는 것이 쉽지 않다. 결국 상인은 플랫폼을 전환하는데 따른 비용이 크기 때문에 쉽게 이탈하지 못한다. (현재 한국의 경우 배민-쿠팡이츠 동시 배달이 가능한 음식점이 대다수라 미국이나 다른 시장에서 ‘독점 계약’이 가능한지 모르겠지만, 가능하다면 결국 플랫폼간 소비자 쟁탈전이 벌어지게 될 것이며, 그 결과에 따라 음식점들이 선택을 하게 될 것이라고 생각한다. 물론 한국과 같이 독점계약이 불가능하다면 음식점들의 전환비용 문제는 크지 않을 것이다)

배달원

배달원들은 DASH에 소속되기 때문에 전환비용이 있다면 강한 해자의 근거가 된다.

현재 DASH는 다음과 같이 근무 시간, 임금 지급 방식 등에 있어 배달원들의 선호를 반영하는 정책(Flexible Pay Model)을 운영하고 있어 배달원들이 진입하기 용이한 환경을 만들어 부업 등 저숙련 배달 노동자들이 일할 수 있는 여건을 마련했다.

개인의 상황 반영 : Dashers는 경력이나 당일 일정, 선호하는 주문 유형에 따라, 즉시 지급 옵션 또는 정산 주기 선택 등 다양한 지급 옵션 중에서 선택할 수 있다. 동기 부여 및 참여 증가 : 이런 선택지는 Dashers가 자신에게 가장 유리한 조건을 선택할 수 있게 해 주어, 플랫폼에 대한 만족도와 지속적인 활동 참여를 촉진한다.

이를 통해 협상력의 강화와 함께 저숙련 배달 노동자들은 다른 일을 할 여건이 되지 않는 경우가 많기 때문에 이들의 전환비용은 낮으며, 결국 배달 조건이 다소 불리해지더라도 이탈할 유인이 적게 된다.

따라서 DASH의 유통망 네트워크는 다소 충격이 있더라도 유연성을 갖추어 견고할 수 있다.

경쟁사는 다음과 같은 이유로 Flexible Pay Model을 도입하기 어렵다. 방대한 데이터와 알고리즘 기반 최적화 : DoorDash는 수년간 축적된 주문, 배달원 행동, 지역별 수요 데이터를 바탕으로 실시간 지급 옵션을 최적화하는데, 이러한 정교한 알고리즘과 운영 프로세스는 경쟁사들이 처음부터 구축하기 어려운 독자적 자산이다. 실시간 데이터 처리 및 분석 인프라 : 배달원들의 주문, 위치, 근무 시간, 선호도 등 다양한 데이터를 실시간으로 수집·분석할 수 있는 클라우드 기반 데이터 플랫폼이 필요하다. 이를 통해 각 Dashers의 상황에 맞는 지급 옵션을 동적으로 제공할 수 있다. 머신러닝 및 알고리즘 최적화 : 배달원 참여율, 작업 패턴, 주문 밀집 지역 등의 데이터를 바탕으로 최적의 지급 조건을 산출하는 머신러닝 알고리즘이 필요하다. 예를 들어, 특정 시간대나 지역의 수요 예측에 따라 지급액이나 보너스 구조를 자동으로 조정할 수 있다. 결제 및 금융 시스템 통합 : 다양한 지급 옵션(즉시 지급, 주기적 정산 등)을 원활하게 처리할 수 있는 금융 기술 및 API 통합 솔루션이 필요하다. 이는 보안과 신뢰성을 유지하면서도 여러 지급 방법을 지원할 수 있도록 설계되어야 한다. 모바일 애플리케이션 및 백엔드 개선 : Dashers가 자신의 지급 옵션을 쉽게 선택하고 확인할 수 있도록, 사용자 인터페이스(UI)와 사용자 경험(UX)을 개선한 모바일 애플리케이션과 이를 뒷받침하는 안정적인 백엔드 시스템이 필요하다. 플랫폼 문화와 내부 프로세스 : 유연한 지급모델은 배달원들의 다양한 상황(예: 근무 시간, 선호 주문, 지역 상황 등)을 반영하여 지급 조건을 동적으로 조정하는데, 이는 DASH의 문화와 관련되어 있어 고정 지급 체계로 운영하는 경쟁사들이 이를 단기간에 전환하기는 어렵다. 실시간 운영 모니터링 및 피드백 루프 구축 : 배달원의 활동과 지급 효과를 실시간으로 모니터링할 수 있는 운영 대시보드와 피드백 시스템이 필요하다. 이를 통해 지급 모델이 실제로 배달원 참여 및 만족도에 어떤 영향을 미치는지 지속적으로 분석하고, 빠르게 조정할 수 있다. 프로세스 표준화 및 자동화 : 지급 관련 프로세스(예: 배달 완료 시 지급 처리, 보너스 산정 등)를 자동화하고 표준화하여 오류를 줄이고 운영 효율성을 극대화해야 한다. 이를 위해 기존의 수동 프로세스를 디지털화하는 혁신이 필요하다. 배달원 교육 및 변화 관리 : 새로운 지급 모델 도입에 따라 Dashers가 변경된 지급 조건과 사용 방법을 숙지할 수 있도록 체계적인 교육 프로그램 및 지원 체계를 마련해야 한다. 이는 배달원들이 새 시스템에 원활히 적응하고, 모델의 혜택을 최대한 활용할 수 있도록 돕는다. 협업과 커뮤니케이션 강화 : 기술팀, 운영팀, 금융팀 등이 긴밀하게 협업하여 지급 모델이 실시간 데이터와 운영 상황에 맞춰 조정될 수 있도록 하는 내부 커뮤니케이션 체계를 통해 시장의 변화에 빠르게 대응할 수 있다.

네트워크 효과

소비자, 상인, 배달원 증가의 선순환

소비자, 입점 상인, 배달원이 증가할수록 사용자 효용이 더 크게 증가하는 선순환이 강화된다.

우선, 소비자가 증가할수록 상인, 배달원은 플랫폼에서 서비스를 제공하면서 더 큰 매출을 올릴 기회가 생긴다. 이에 따라 다양한 서비스가 신속하게 제공될수록 소비자들의 만족도가 높아진다.

크로스 셀링 : Uber eats, Instacart가 모방할 수 없는 사업 구조

또한, 카테고리가 확장될수록 원래는 수요가 없었던 신규 소비자들이 앱에서 추천해주는 상품이나 서비스를 보고 주문을 해보는 크로스셀링 효과가 발생한다.

다양한 경로로 들어오는 신규 고객 대상으로 용이하게 광고효과를 높일 수 있으며, 이러한 효과는 MAU의 25%가 식료품 등 음식 배달 외 새로운 카테고리의 주문을 했다는 점으로부터 확인된다.

또한, 카테고리에 따라 배달이 몰리는 시간이 다르기 때문에 다양한 카테고리로 확장이 잘 된 경우, 유통망, 특히 배달원 고용상의 유리함이 크다.

음식료/유통 브랜드와 협업 : 미국 내 지배적 사업자의 우위

DASH는 미국 음식료 배달 시장의 지배력을 바탕으로 월마트, 스타벅스 등 글로벌 브랜드와 협업을 진행중이다.

이러한 입점 브랜드가 늘어날수록 지역적으로 확장할 경우에도 이들 브랜드와 협업하여 빠르게 점유율 확대가 가능하다.

그리고 이들 브랜드 입장에서도 배달 앱을 사용할 인구라면 구매력이 보장되기 때문에 신규 시장 개척에 유리한 채널이라는 점에서 신규 지역에 런칭할 때에도 입점하는 것이 유리하다.

결국 글로벌 유통 기업 입장에서도 네트워크 효과가 발생한다.

낮은 생산비용

핵심 생산 자산에 대한 독점적 접근권

DASH는 다양한 국가에서 플랫폼을 운영하면서 행동경제 실험에 가까운 소비자 데이터 통계를 보유하고 있다. 이런 데이터를 축적할수록 AI를 활용하여 경로 최적화, 소비자 수요예측을 정교하게 할 수 있다. 이러한 데이터에 대한 독점적 접근권을 바탕으로 다른 회사는 추구할 수 없는 운영상의 효율성을 달성할 수 있다.

규모의 경제

높은 고정비가 분산된다.

플랫폼 운영, 마케팅, 기술개발 등 고정비용은 주문량과 무관하게 발생하므로, 주문량이 늘어나면 고정비가 분산된다. 또한, 주문 데이터가 축적될수록 AI를 활용하여 경로 최적화, 소비자 수요예측이 정교해져서 운영 효율성이 향상된다.

변동비도 지역내 카테고리, 주문 빈도, 주문량 확대에 따라 매출이 증가하면서 줄어든다.

1. 기사들의 배달 효율화 : 주문이 증가하면 비슷한 경로의 주문을 묶어 한 번에 여러 건을 배달하는 묶음 배달이 가능해져서 배달원당 처리건수가 증가하고, 연료비, 시간당 비용이 절감된다. 2. 기사 활용도 개선 : 주문 증가로 작업이 꾸준해지면 유휴 시간이 줄어 임금 효율성이 높아진다. 3. 협상력 강화 : 플랫폼은 영향력이 커지면 유리한 조건으로 배달원과 수수료 협상을 할 수 있다.

이익률(협상력)

24.4Q 실적발표로 DASH가 입증한 성장성

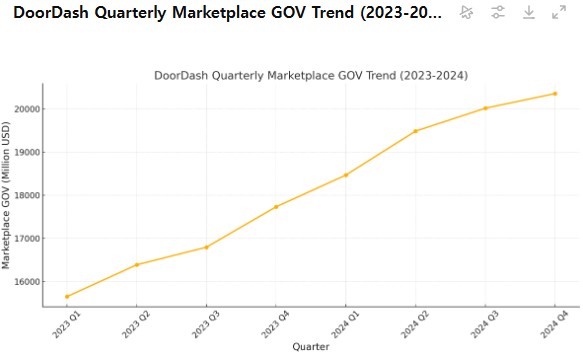

YoY 기준 주문건수는 6.85억건(+19%), 총 주문액(GOV)은 $213억(+21%), 매출은 $29억(+25%), GAAP 순익은 $1.41억(흑전), EBITDA는 $5.66억(+55.9%)이었다. (총 주문액 증가율이 더 높은 것은 소비자당 주문량의 증가를 의미하며, 이보다 매출, EBITDA가 더 크게 증가한 것은 수수료율이 더 개선되고 비용은 덜 증가했다는 높은 협상력을 입증한다)

또한, 월간 활성 사용자수는 4,200만명(+13.5%), DashPass(유럽 자회사 Wolt+) 회원수는 2,200만명(+22%)을 넘었다.

가격설정력

지금까지의 성장 내러티브에 따라 DoorDash 플랫폼을 사용하는 유저 수가 증가할수록 상인들에 대한 협상력이 강화되어 수수료율, 광고료가 증가할 수밖에 없다. 이는 GOV 증가율보다 매출 증가율이 더 높은 것으로부터 확인할 수 있다. 전체 주문액에서 매출로 인식되는 비중이 높아진 것이다.

거래량 확장

GOV는 코로나 이후 ‘24.4Q까지도 꾸준히 성장하고 있다. 음식 배달 시장은 성장률이 둔화되겠지만, 초기 단계인 다른 지역, 다른 카테고리의 성장률이 전체 성장률을 견인하고 있다.

비용 감소

DASH는 배달원 배송비를 낮추고, 배송을 효율화하여 유통 비용을 감소시킨다. 특히, 유연한 근무 시간 선택, 시간당 보상 등 다양한 조건으로 배달원과 계약을 체결하여, 신규로 배달원이 될 때의 진입장벽을 낮추고 더 많은 잠재 배달원을 확보하고, 결과적으로 플랫폼의 협상력을 높이는 데 기여한다.

이는 배송 효율화, 고정비 분산, 규모의 경제 효과로 인해 가능했으며, 23.3Q 컨콜 당시 CFO는 직전 4분기 동안 매출이 25~30% 이상 성장하는 가운데 영업비용이 상대적으로 평탄하게 유지되었다고 언급하였다.

자본배치

R&D

DASH의 CEO Tony Xu는 23.1Q 컨콜을 통해 다음 분야에 적극적으로 AI 기술을 도입하여 소비자, 상인, 배달원에게 더 나은 플랫폼 이용 경험을 주기 위해 노력하고 있다고 언급하였다.

1. 상품 카탈로그 자동화 : 오프라인 매장의 제품 정보를 디지털화하는 과정에서 AI를 활용해 빠르게 상품 데이터를 구축 2. 소비자 맞춤형 추천: AI를 이용해 사용자의 과거 주문 이력을 분석하고, 선호하는 음식 및 제품을 추천 3. 고객 지원 자동화: AI 챗봇을 활용해 고객 문의 대응 속도 및 정확도를 개선 4. 배달 최적화: 머신러닝 기반으로 예상 배달 시간, 최적 루트, 다중 주문 처리 등을 개선하여 배달 품질 향상

광고

필요한 경우 적극적으로 광고를 진행하여 소비자, 상인, 배달원 증가에 따라 네트워크 효과가 발생하여 선순환이 일어날 수 있도록 하고 있다.

이러한 광고에 대해서도 DASH는 내부적으로 시장에서 비용이 회수되는데 걸리는 기간을 ‘Payback period’로 설정하고 이를 달성하고 있다고 언급하고 있다.(23.4Q 컨콜)

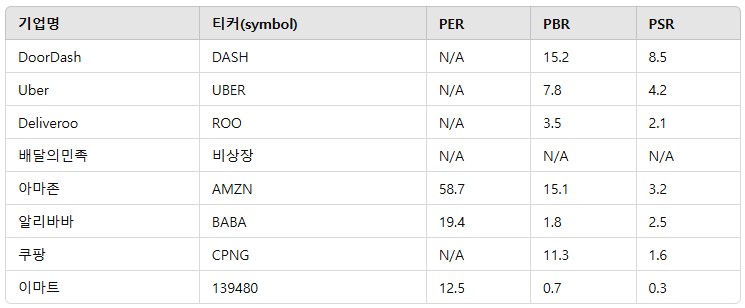

밸류에이션

아래 표를 보면 다른 플랫폼 기업에 비해 멀티플 측면에서 다소 비싸다는 평가가 가능할 것 같다.

하지만, 높은 성장성, 다변화된 카테고리에 따라 발생하는 크로스셀링 효과, 주요 시장이 아직 초기 단계인데도 수익성을 달성했다는 점, 이를 바탕으로 지역적 확장을 적극적으로 해나가고 있다는 점 등을 고려할 때 충분히 프리미엄을 줄 수 있는 상황이라고 판단된다.

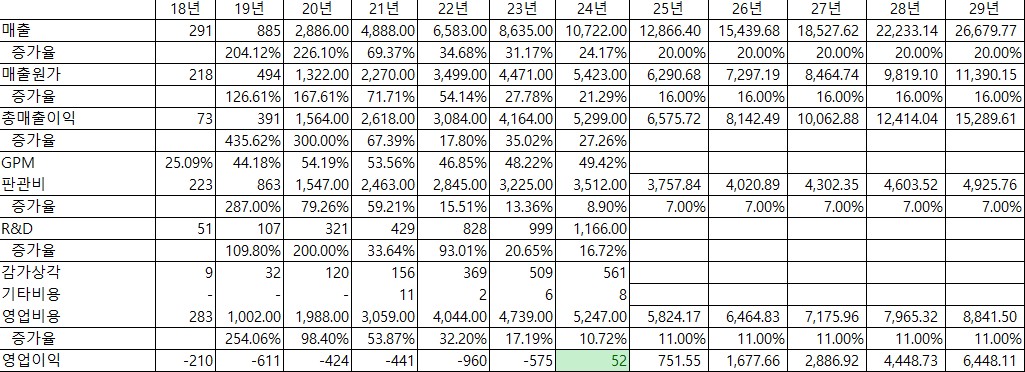

나는 전 세계 음식 시장 기대 성장률 10%과 향후 소비자 편의성 추구에 따라 증가할 온라인 배달 시장 침투율, 카테고리 확장 효과와 지역적 확장 효과를 감안하면 상당 기간 동안 매출 성장률은 YoY 20% 수준을 유지할 것으로 기대한다.

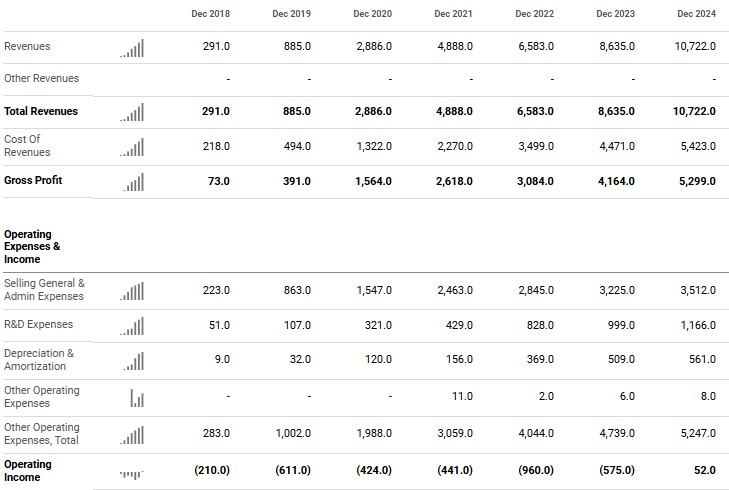

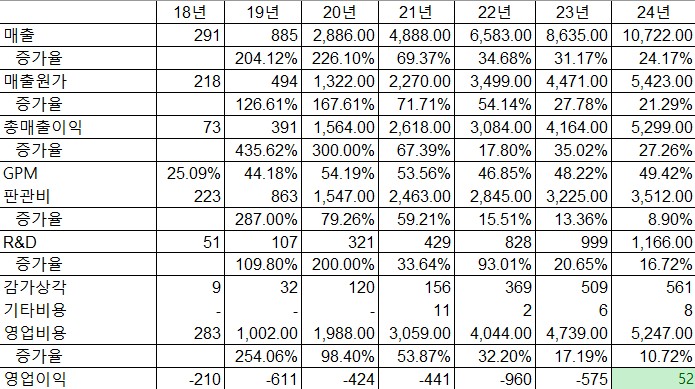

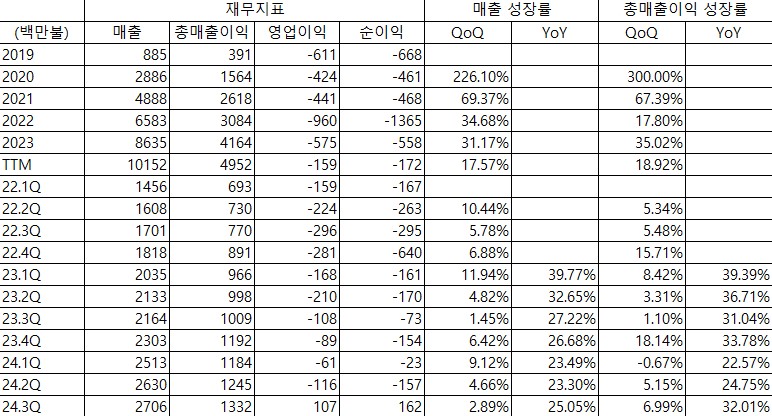

또한, 위 7년간 재무지표를 보면 매출 증가율과 비교했을 때 매출원가 증가율은 5%p, 판관비 증가율은 16~19%p, 영업비용 증가율은 2~14%p 정도 낮은 수준으로 유지되고 있다.

보수적으로 매출 증가율이 20%, 매출원가 증가율이 4%p 낮은 16%, 판관비 증가율은 13%p 낮은 7%, 영업비용 증가율은 9%p 낮은 11% 수준에서 5년 정도가 경과된다고 가정해보면, 영업이익이 ’25년에는 $7.5억, ’27년에는 $28.9억, ’29년에는 $64.5억으로, 현재 시총 $800.8억을 기준으로 POR은 ’25년 106.6, ’27년 27.7, ’29년 12.4이다. 갑자기 현실적인 멀티플이 된다.

사실 현재 성과로 증명한 DASH의 성장성을 감안하면 상당히 보수적인 기대치라고 생각된다. 회사가 의도적으로 보다 적극적으로 R&D, 광고 투자를 늘린다면 수익성은 다소 낮아질 수 있겠지만 매출 성장성은 더 확대될 수 있을 것이라고 생각되며, 이것이 아마존이 추구해온 전략이었다.

이러한 관점에서 DASH는 고평가되지 않은 성장주로, 시장이 비싸다고 생각할 때 담아두면 오랜 기간 동행할 수 있는 기업이라고 생각한다.

S&P 500 편입 효과(feat. Chat GPT)

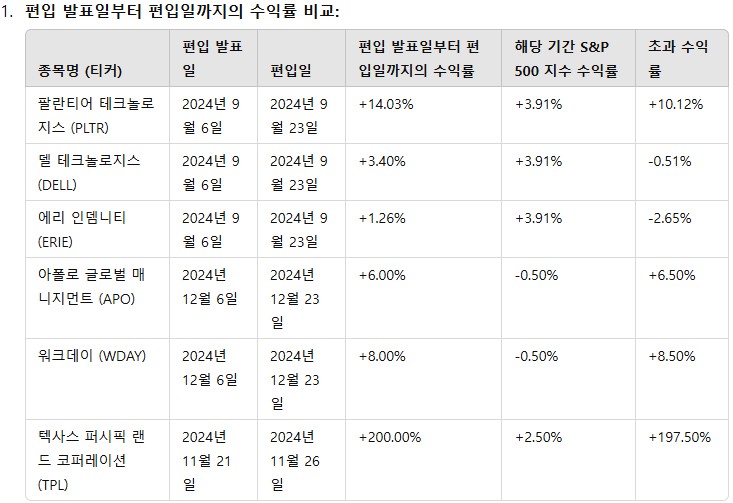

DASH가 S&P 500 지수에 편입된다는 뉴스가 3.10일 발표되었다.

오는 월요일인 3.24일이 편입일이므로 편입일까지 수익률을 구해보면 7.19%이다. 해당 기간 S&P 500 수익률은 5,614.56에서 5,667.56으로 0.94%, 초과수익률은 6.25%이다.

과거 편입종목의 편입일까지의 초과수익률을 보면 TPL의 극단적 사례를 제외하면 DASH와 대동소이한 수준이다.

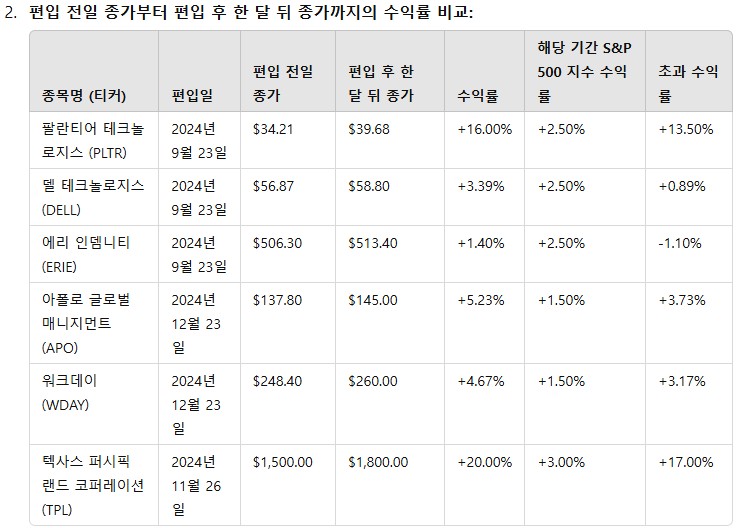

그리고 편입 한 달 뒤까지 초과수익률을 보면 다음과 같다.

결국 기업이 얼마나 사업을 잘 하느냐가 가장 중요하다. 다만, 상당 기간 동안 시장에서 억울한 일을 당할 위험은 낮지 않을까?

가치투자 커뮤니티를 성장시켜나가고 있습니다. 운영 계획과 방향성을 한 번 읽어보시고, 텔레그램과 유튜브 채널을 통해 소통하고 있으니 공감이 가신다면 참여해주세요! 쌍방향 소통을 원하는 분들은 카카오톡 채널로 와 주시면 좋을 거 같습니다. 자료실을 통해 리포트, 뉴스도 공유하고 있으니 참고하시면 도움이 될 거 같습니다.

DoorDash가 티커대로 상방으로 DASH하고 있다. (예전 분석 글도 참고) 24.3Q에는 흑자 전환까지 이뤄내며 파죽지세다.

아직까지 시총 대비 이익 규모가 의미있는 수준은 아니며(연환산 PER 100 수준), 플랫폼 사업 특성상 규모의 경제와 내러티브가 중요하기 때문에 재무지표는 간략하게 살펴보고, DoorDash가 그리는 성장 내러티브를 보여주는 질의응답을 자세히 살펴보도록 하겠다.

엔믹스 DASH 한 번 듣고 가실께요~(입덕 영업 죄송;)

DoorDash 성장성을 보여주는 24.3Q 재무지표

24.3Q 흑자 전환, 성장 추이

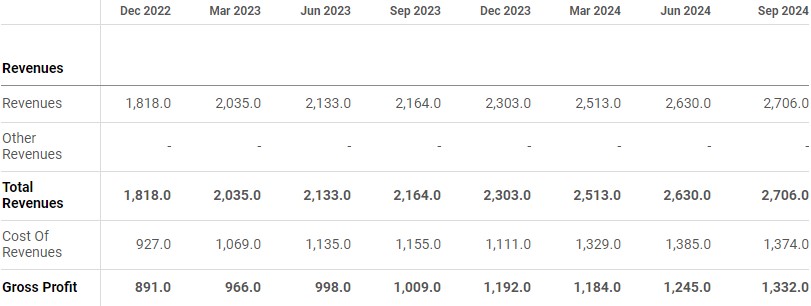

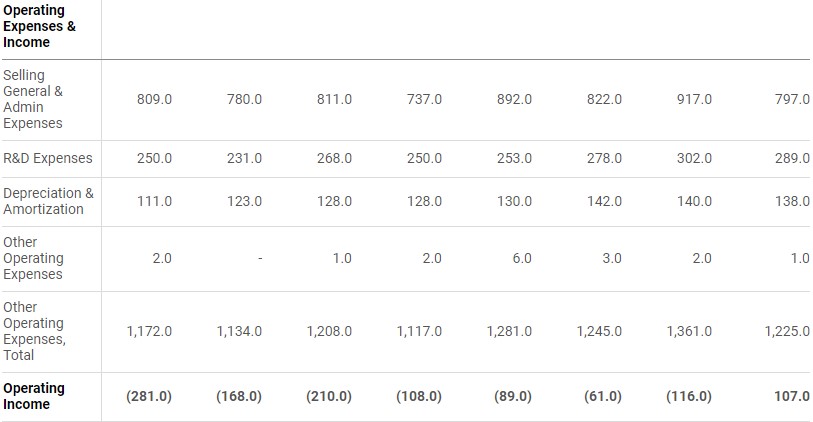

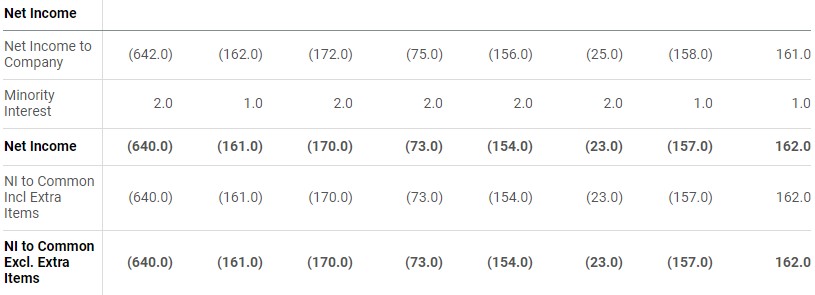

미국 현지시각 10.30일 저녁(한국 시간 31일 새벽) DoorDash 24.3Q 실적이 발표되었다. 매출이든, 이익이든 정말 거침없는 성장세이다. 24.2Q YoY 성장률이 23.3%였는데, 24.3Q YoY 성장률은 25.0%로 더 기울기가 급해졌다. (오른쪽으로 갈수록 최근 실적)

영업이익은 최초로 흑자로 전환하였다. 인상적인 것은 매출의 급증 가운데 원가가 감소하고 있다는 것이다.

그간의 실적을 살펴보면, 매 분기 매출과 총매출이익 성장을 이뤄왔으며, YoY 기준 성장률이 계속 20%를 초과해왔음을 확인할 수 있다.

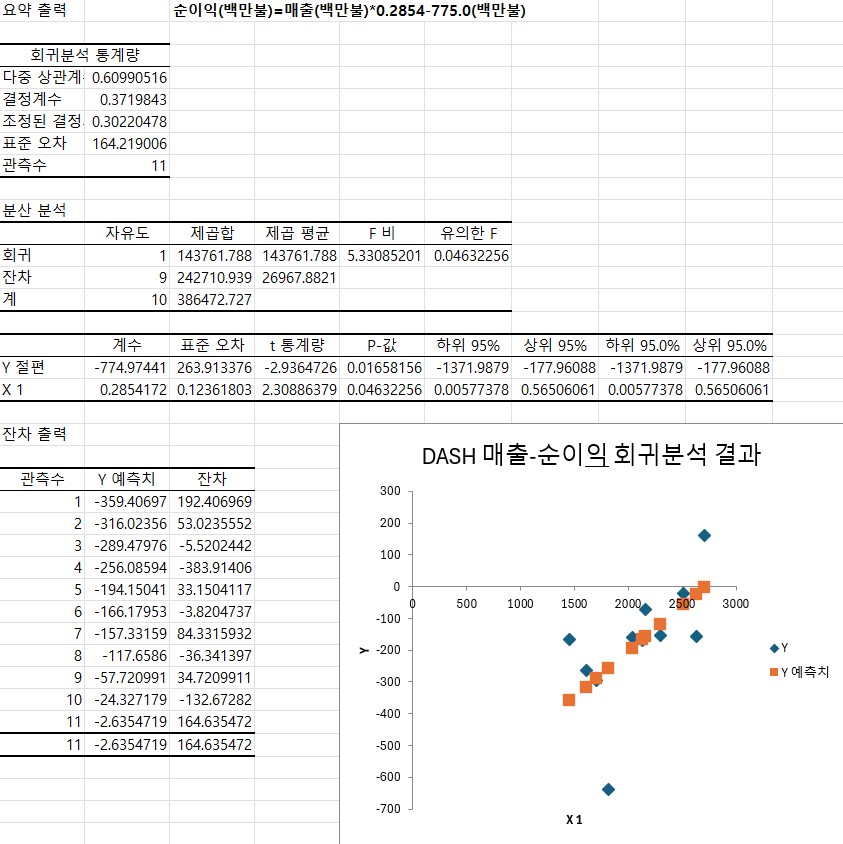

그리고 긴 성장의 끝에 24.3Q에 드디어 영업이익과 순이익이 흑자전환했음을 확인할 수 있다. 매출 성장에 따라 어떤 추이로 이익이 개선되는지 확인하기 위해 회귀분석을 해봤다. 순익(백만불)=매출*0.2854-775.0(백만불) 으로, 고정비는 7.75억불, 매출 성장시 장기 순이익률은 28.5% 수준에 수렴하게 될 것으로 예상되며, YoY 성장세가 유지되면 25.3Q 순익은 2706*1.25*0.2854-775.0=190.4(백만불)로 예상된다.

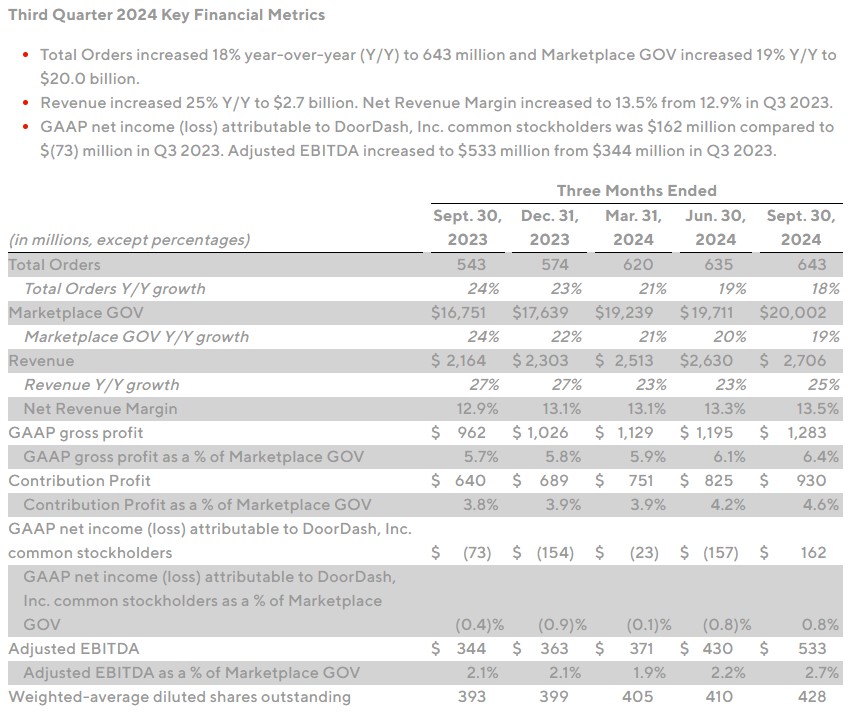

자신감의 표현일까, 재무지표를 보도자료로 배포하고, 컨콜 시간을 모두 Q&A 세션으로 채웠다. 주요 질의 응답을 정리하여 DoorDash의 영업 현황을 파악해보도록 하겠다. (내용을 정리하고 참고용으로 아래 영어 원문을 표시, 결론에 전체적인 내러티브 평가)

DoorDash 24.3Q 질의 응답

회사측 참가자 : Andy Hargreaves(IR 담당 부사장), Tony Xu(CEO), Ravi Inukonda(CFO)

Nikhil Devnani(Bernstein) : 해외사업 성장추이, 고정비 질의

미국 사업에서 소비자 집단이 서비스를 경험하고 3~4년이후 수익성이 개선되었는데, 해외사업도 유사한 추이인지, 아니면 시장 구조 등 원인으로 인해 다른지? I wanted to ask a two-part question on international. So in the past, you’ve kind of illustrated this dynamic in the U.S. business where as cohorts experienced go forward and mature a little bit you see improvements in the contribution margins by years three and four. Now that you’ve been operating in some of these international markets for a few years now, have you seen a similar arc and magnitude of improvement on the contribution margin front for these cohorts as well? Or is it a little bit different for market structure reasons or for other reasons?

해외 사업 운영시 미국 사업에서의 기술과 인력은 공유할 수 있겠지만 배달은 매우 지역 기반 사업이라는 점을 고려할 때 해외 확장 과정에서 고정비 부담이 완화될 수 있는지? And then my second question is around the degree of fixed cost leverage that you can get operating in so many different countries at once. I’m sure you get to share some technology and talent, but given delivery is hyper local, how do those two things shake out? Is your fixed cost burden in your newer markets lower and easier to overcome or not really? Thank you.

CEO : 미국 DoorDash와 유사한 추이로 점유율 확대, 시장/제품 추가시 같은 팀이 작업하여 확장 노하우 레버리지 발생

매출, 이익측면에서 미국과 해외 시장은 비슷하다. Volt(DASH가 인수한 해외 배달사업 회사)와 처음 협업할 때 미국 사업과 유사한 유지율, 주문빈도 데이터를 볼 수 있었고, 효율적 성장 경로를 반복할 수 있다고 본다. Hey, Nik, it’s Tony. I’ll start and Ravi feel free to chime in here. I think on your first question, in short, the answer is yes. We are seeing similar progress both top line and bottom line in our international markets that we saw, while building the U.S. And that’s because if we were to rewind the clock three years ago when we first partnered with Volt, what we saw in the company was something that looks very familiar to us at DoorDash, which is a company that has built the leading product when it came to retention and order frequency. And that really is what drives the flywheel in terms of efficient growth.

진출한 모든 시장에서 점유율과 수익이 올라가고 있다. And so we continue to see this past quarter as well as in the last several years of partnering together with both continued strong progress, where we virtually are gaining share in every single market that we play in. and we continue to see the bottom line perform in tandem. And so you are seeing that progression, and it’s been very encouraging.

고정비와 관련된 두 번째 질문 관련, DoorDash는 후속 시장/제품을 추가할 때 동일한 팀이 작업을 진행하기 때문에 확장 노하우 측면에서 영업 레버리지가 발생한다. I guess, I can start on the second question, and then I’ll hand the mic over to Ravi. In terms of fixed cost leverage, in short, the answer is yes. As we add subsequent markets or subsequent even products, we do use, I mean, for all intents and purposes the same team. You’re right to say that these are hyper local businesses and services. So we do have to obviously start new in terms of acquiring each of the different audiences. But in terms of the tech stack, in terms of the products, in terms of the know-how whether that’s expanding products within a geography or adding net new geographies, you do see that operating leverage.

CFO : 경쟁사보다 빠른 성장, 규모의 경제 효과

해외사업은 24.3Q 뿐만 아니라 24년 동안 계속 성과가 좋았으며, 경쟁사들보다 빠르게 성장하여 모든 진출 시장에서 점유율을 확대했다. Yes. Hey, Nick, let me add a couple of points there, right? Like when you think about the performance of the overall international business. I mean, it has a strong third quarter as well as the year itself has been very strong. When you think about it from a growth perspective, we are growing substantially faster than peers, which essentially means we’ve gained share in virtually most of the markets that we operate in.

24.2Q 총매출이익이 흑자이며, 24.3Q에도 그렇다. 규모의 경제가 작용하는 사업이며, DASH는 유지율과 주문빈도를 높일 기회가 있으면 두 배로 투자한다는 원칙에 따라 경영해왔다. Last call, if you recall, I mentioned the fact that the overall international business is gross profit positive. It continues to be the case. The dynamics are similar, right? Like this is a scale-driven business. Our goal has always been, if we find good opportunities to drive retention and order frequency, we’re going to double down and invest. That’s the same formula we are using in the international market. We are pleased that the gross profit continues to improve.

미국 사업과 마찬가지로 규모의 경제가 중요하며, 해외사업이 초기 단계라는 점을 고려했을 때 고정비 측면에서 유사한 추이를 보일 것으로 기대한다. On the fixed cost, I mean, similar dynamics that we saw in the U.S. Again, a lot of it has to deal with scale. But if you recall where we are in the international markets, we are still very early. We’re investing behind product, and that’s what’s causing the strength that you’re seeing from a cohort retention and an order frequency perspective.

Michael Morton(Moffett Nathanson) : 식료품 성과, 이용자 특성

식료품 유통사들이 DASH 플랫폼에 접근하고 있는지? 식료품 분야 쇼핑 시간, 쇼핑 액수 등 추이를 공유해줄 수 있는지? Hi, everyone. Thanks for the question. I wanted to start firstly maybe one for Tony, and then a cohort question for Ravi. It’s great to see the Wegmans grocery announcement. Just curious if we’re getting closer to seeing an unlock of some of the largest grocers in the country who are not currently on DoorDash platform coming on to DoorDash? And then on the grocery topic and thinking longer term and your ability to make strides into the market. Could you talk about the trends that you see for the grocers who have been on the platform for the like longer extended period of times that you see with larger baskets and maybe larger basket market share trends for the grocers have been on the platform for two years?

DASH 이용자 집단의 특성(연령대)에 대해 공유해줄 수 있는지? And then for Ravi your comments on cohorts the last couple of quarters is really encouraging. The new cohorts coming in being as strong as ever. The question that we get from investors is, who are these people? What are the demographics isn’t everybody already ordering food and clearly not? So we would love if you could maybe shine a little light on what they look like. Is this skewing younger college age students, more digitally inclined, who are moving out of their home every fall going to college? Anything there would be great. Thanks again.

CEO : 수요 충족에 집중하여 이용자/주문량/빈도 증가

4년 전 자주 소비하는 품목, 주 중간에 소비되어 새로 구입이 필요한 식료품 구입 수요를 충족하기 위해 식료품 시장에 진출했다. Hey, Michael, it’s Tony. Yes, on the first question related to grocery, we’re pretty excited about what we’re seeing in grocery. I mean, we launched grocery at this point almost four years ago now. And the entry point was by delivering a product that was relatively speaking, new to the market, which was solving for this top-up experience, where for consumers, we were replenishing that middle of the week run where you run out of the items that you consume the most often or the earliest or the ones that perish the most frequently, whether that’s your berries, your fruits, your dairy products, your coffees, et cetera.

새로운 카탈로그를 만들고, 수요 품목을 충분히 이해하여 이용자들이 이해하기 쉽고 기존 식료품점에서 할 수 없었던 것들을 가능하게 하는데 시간이 걸렸고, 아직도 해결이 필요한 문제이다. And I think what that spurred was both an introduction that was easy to understand for consumers and also something that grocers hadn’t seen before and made it very easy to onboard a lot of these grocers. Now all of these things take time, right? I mean we had to build a new catalog from scratch. We obviously wanted to make progress on understanding inventory and the reliability of the inventory fees that we’re receiving, which we thought is one of the biggest problems to solve here.

DASH는 미국 최대 식료품점들을 포함하여 큰 진전을 이뤘고, Wegmans 뿐만 아니라 모든 식료품점 입점을 동등하게 반기고 있다. And we’ve made tremendous progress pretty much across the Board, whether that’s adding selection, including some of the largest grocers in the country. We’re just as excited as you are about Wegmans, but also everyone else that whether that’s the corner grocery store to the middle market, grocery stores. And I think this is why you’re seeing, when it comes to customer adoption, customers come to DoorDash first, new customers into the grocery delivery industry. And just in general, to delivery outside of restaurants come to DoorDash first, before any other platform.

이용자들도 식료품을 DASH에서 사는데 익숙해지고 있으며, 점점 더 많이, 자주 사고 있다. And so I think you’re already seeing a lot of this. And in terms of other trends, we see that as customers get used to ordering groceries on DoorDash, they tend to order more items each subsequent visit. So from a cohort perspective, you’re noticing that we are increasing both the frequency as well as the spend and wallet share in terms of how consumers spend when it comes to their monthly bills on grocery. And that’s increasing with every single cohort.

결국 초기 기대보다 더 시장이 커졌고, DASH는 신규 이용자 확보가 일어났는지, 점유율을 선도하고 있는지, 구매가 유지되는지, 경쟁기업을 따돌리고 있는지 모니터링하고 있다. So in short, I think what we’ve seen is, we have seeing a much bigger market than we expected when it came to launching this pop-up run product, which now has nicely translated into shopping for the other types of occasions, including your weekly stock ups and those types of baskets. And we just continue to see whether it’s on the new customer acquisition side, leading share there. And then also on the retention side, positioning us to really continue to grow in a way that will outpace others as well as outpace our previous cohorts.

CFO : 기존 이용자, 식료품 신규 구매 등 이용자 증가 경로 다변화

대부분 고객은 기존(배달을 이용하던) 이용자로부터 나온다. Hey, Mike, it’s Ravi. I’ll take the one on cohorts side? Maybe I’ll just level up and give you broadly on what we’re seeing from an underlying cohort perspective. I mean, you’re right, we’ve been very pleased with the cohorts. I think about it like a majority of the volume still comes from existing cohorts for us. The most instructive thing for me when we’re operating the business is to look at the engagement of the older cohorts.

하지만 5~7년 이상 된 이용자들도 유지되며 구매를 증가시키고 있다. And if you look at the older cohort, even cohorts as old as five, six, seven years old, we’re still seeing good amount of retention as well as overall wallet share increase. And that tells you that the improvements we are making in the product, whether it’s selection, whether it’s adding new categories, all of that is driving the new, I mean, the cohort trend that you’re seeing in the business.

또한, DASH는 여전히 새로운 이용자를 유인하고 있으며, 연령대 측면에서도 그런데, 이는 DASH가 더 많은 선택지, 식료품 등을 추가하며 변하고 있기 때문이다. From a new cohort perspective, I’ll have a couple of ways to think about this, right? One is we’re still attracting a healthy amount of new consumers. It’s not any different from a demographic perspective. We’re starting to see cohorts coming from some of the suburban markets still. And the reason for that is, remember, this is a product that continues to change. We add more selection, grocery, in many cases, the selection is net new to the platform.

또한 최근에는 식료품 구입으로도 이용자들이 유입되고 있다. And the second way we are seeing is not only are consumers new to restaurants, today, we actually add consumers that start their journey with grocery as the first order. That’s a net new consumer that we’re adding to the platform. But overall, when I look at the underlying cohorts, I mean the strength continues to be very strong, both across existing as well as new.

Bernie McTernan(Needham & Company) : 타사 협업 전략

협업 전략은 어떻게 되는지? Great. Thanks for taking questions. Just wanted to ask about the partnership strategy, especially in light of the list announcement from tonight. So maybe just talk about the broader partnership strategy. I know you also partner with streaming companies, for example, but is there anything different here with the list that there is the driver component as well?

CEO : 좋은 제품 제공을 통한 유기적 성장이 우선(80%), 협업도 좋은 고객 확대 기회(20%)

DASH가 가장 중요하게 생각하는 것은 상권을 활성화하는 것이다. 따라서 이용자들에게 선택권, 품질, 경제성, 서비스를 제공하기 위한 제품 구성을 중요하게(80%) 생각한다. 이런 노력이 있었기에 Dash 패스가 성공할 수 있었다. Yes. Hey, Bernie, it’s Tony. Maybe I can take this one. So one of the things we have at DoorDash that we believe in and follow religiously, is that we keep the main thing, the main thing. And the main thing at DoorDash is building and enabling local commerce. And so when you think about kind of our perspective on all things, partnerships as well as building products, the 80 goes towards building products, which means that it’s because that we’ve offered customers the best combination of selection, quality, affordability and service that we get used the most often our app. And because we get used the most often, it’s how we actually are able to build not only the most useful, but also the largest local commerce membership program, which is Dash pass.

20%는 협업으로, DASH 네트워크 밖에서 이용자들에게 매력적인 혜택을 제공할 수 있는 기업들이 있다. Chase, MAX 등 회사와 협업을 발표했고 오늘 Lyft와의 협업 발표는 정말 기대된다. Now that’s the 80. The 20 is the partnerships piece, where for us, we do believe that there are others outside of our network that can offer attractive benefits to our members. You saw this a few years ago when we first launched our partnership with Chase, which we renewed in an expanded way earlier this year. Then you saw the announcement and partnership with MAX, which happened a couple of months ago in terms of adding streaming benefits to DashPass subscribers. And then today’s announcement with Lyft, which we’re really excited about.

Lyft는 수백만 라이더가 이용하는 서비스이며, 다수는 이미 DASH의 고객이다. 많은 사람이 추가로 DashPass 회원 가입할 기회라고 생각하며, Lyft 입장에서도 가장 큰 지역 상거래 플랫폼에 접근할 수 있게 되어 매력적인 협업 기회이다. Lyft is a service that’s used by millions of riders. And many of those riders already are DoorDash customers. Some of them are DashPass subscribers, but a lot of them are also not DashPass subscribers. And so I think it’s a great opportunity for us to continue to add engagement to the DashPass program as well as new DashPass members. And in return, lift gets access to the largest local commerce platform that sees the highest frequency program of its kind when it comes to consumer membership programs. And so I think that will be great for them as well.

하지만 80%에 해당되는 유기적 성장의 기회는 아직 많이 남아 있다. But again, the 80 for us remains to be building the products. And if you think about it, the runway for just organic growth, for DashPass, or really just for our own customer base is this quite large. I mean we have hundreds of millions of customers who order with us every year, whether it’s on DoorDash or on Wolt and only a fraction of those are members to either DashPass or Wolt+. So we’ve got a long ways to go just within our own ecosystem.

아직도 외식업에서 비중은 한 자릿수이며, 따라서 가장 중요한 것은 제품을 개선하여 이용자수, 가입 회원수를 늘리는 것이다. And then when you look at this from the consumer’s perspective, although we’ve done a reasonably good job in terms of enabling local commerce in the categories that we play in today, we still only represent single-digit fraction of the restaurant industry and a much smaller fraction of that outside of restaurants. So I think there’s a long runway ahead, and the main thing for us continues to be improving our products so that we can be the most useful to customers that they use our products most often, which will give us the privilege of having them as members in our programs.

Shweta Khajuria(Wolfe Research) : 수익성 개선 요인, 목표 배송비 수준(경쟁 목표 기업)

수익성 개선 요소로 광고 성장, 플랫폼 기여도, 비용 효율화를 언급했는데 어떤 요소가 가장 크게 기여하고 있는지? Thank you so much for taking my questions. Let me try two, please. Ravi, the day rate contributors in the past, you’ve mentioned its ad growth and platform contribution as well as cost line efficiencies. Could you maybe please rank order them in terms of the impact on take rates as you think about maybe near to midterm?

중장기적으로 가게에 가서 사는 것만큼 가격이 싸질 수 있다고 보는지? 아니면 경쟁사 수준이 되는 것이 목표인지? And then on price parity, either Tony or Ravi, where do you think you want to be when it comes to grocery price parity in the mid-to-long term. Is there a future where it’s going to be the same as in-store prices? Is that the goal? Or is it that you want to be the most competitively priced online grocery delivery platform? Thank you, Tony.

CFO : 24.3Q 광고 성장, Dasher 비용 절감, 다만 제품 개선이 근본적 원인

매출 성장이 총주문매출(Gross Order Value) 성장을 앞지르고 있는 것은 광고 때문이며, 이는 플랫폼 사업이라는 특성 때문에 가능했다. Hey, Shweta, it’s Ravi. I’ll take the first one on the take rate, right? Let me start by just giving a broader framework around the interplay between revenue and GOV in our business. I mean if you think about revenue, it’s been outpacing the GOV growth in our business. That’s being driven by ads, as you mentioned, it’s been driven by benefits that we get from the commerce platform.

그리고 비용 효율성이 개선될 때마다 수익이 창출되어 매출 성장률이 GOV 성장률을 앞지르게 되었다. 24.3Q에는 광고와 Dasher 비용 절감 효과가 일어났다. 광고는 특별한 변화 없이도 점진적으로 개선된 것이다. And any time we improve efficiency on the cost line, whether it’s cash or cost or CLR, that drives revenue. So that’s why revenue growth has been outpacing our GOV growth rate. And more specifically, what we saw in the third quarter was two things. One is advertising, and the second one is leverage from Dasher costs. I wouldn’t read into the advertising as something has changed in which we operate the business. We are operating the ad business with the same amount of discipline. It’s growing in a very healthy manner.

DASH는 Dasher 측면에서도 제품 개선으로 인해 비용이 절감된 데 대해 만족하고 있다. 매출이 GOV 성장률을 앞지르겠지만, 좋은 투자 기회를 찾게 되면 유연하게 투자할 것이다. We’re also very proud of the leverage that we’ve generated on the Dasher side. A lot of that is being driven by the underlying improvements we are making on the product, and we are pretty happy with that. More broadly, when I think about on a go-forward basis, I would expect revenue to continue to outpace GOV growth. But I would not think of it linearly in terms of the same amount every single quarter. So if you think about the operating philosophy for us, when we find good opportunities to invest, we want to invest flexibly up and down the P&L. Sometimes those opportunities are going to present themselves in the revenue line. And we’re pretty happy to take advantage of that.

CEO : 현재는 정확히 원하는 상품 제공이 더 중요

이용자들은 가격만 보지 않을 것이다. 현재 식료품 사업의 문제는 이용자가 원한 상품을 정확히 받지 못했는데도 추가 요금을 내야 한다는 점이다. DASH는 정확한 상품을 제공하는 것을 우선순위로 두고 있다. Hey, Shweta, it’s Tony. On your question on price parity, I think it’s a good one. I do think though, in the eyes of the consumer, they think about grocery delivery against a few dimensions at the same instance, and it’s not just about price, right? One of the challenges you see in the grocery delivery industry right now is that customers are asked to pay a premium even though they don’t get exactly what they ordered. And that’s one of the key problems that we’re trying to fix here at DoorDash, which is, first and foremost, how do we get customers exactly what they order.

하지만 가격도 중요한 고려 요소이다. DASH는 가능한한 저렴한 가격을 유지하기 위해 소매상들과 협업하고 있으며, 매장 가격 수준으로 제공되고 있는 곳도 있다. 다만, 더 진전을 이룰 수 있다고 생각하며 고객 스스로 사는 것보다 빠른 수준의 편의성 제공도 목표로 하고 있다. We think that we’re making great strides against that dimension. But there are other dimensions. Price is one of them, and we are working with each one of our retail partners to making sure that we do have prices as competitive and affordable as possible. We do have some partners already there in terms of having or matching in-store prices. But we think that we can do more there. And at the same instance, we have to continue to offer the level of convenience where we can be faster than what a customer can do on their own.

결국 주문한 것을 정확히, 기대한 가격으로 더 빨리 얻는 것이 DASH의 목표이다. And so I think the combination of those three things of getting people exactly what they ordered at prices that they would expect, certainly faster than they can do it on their own. That’s kind of what we’re going for. It is the combination of those things in which we’re shooting for.

Cameron Lynch(Deepak) : GOV, AOV 성장 원인

경쟁사보다 높았던 24.3Q 19%의 GOV 성장 요인을 상세히 설명해줄 수 있는지? 또한 평균 주문액(AOV : Average Order Value)이 증가하는데 이는 상품 구성 변화 때문인지 아니면 인플레이션 때문인지? This is Cameron Lynch [ph] on for Deepak. Just two quick questions. First, can you help us unpack the 19% GOV growth we saw this quarter, a high level between core restaurant and other categories such as grocery, either qualitatively or quantitatively? And second, we saw that AOV trends were up slightly this quarter. Is this due to product mix or bed new price inflation. I would appreciate any additional color you can provide on what’s driving this dynamic? Thanks.

CEO : 선택권, 품질, 경제성에 집중하여 이용자, 주문빈도 증가, 외식, 식료품, 해외 부문 모두 성장중, AOV는 식료품 성장이 기여

DASH에게 가장 중요한것은 이용자 추이이다. Hey, Cameron. I’ll take both of those. I mean look, I mean, we’re really pleased with the performance of the business on the growth side. So let me talk about the inputs, and then I’ll talk a little bit about the outputs and the various drivers in the business. From an underlying input perspective, right, I mean, the biggest thing for us is looking at the underlying cohorts.

이용자가 두자릿수로 증가하고 주문빈도도 지속 상승하여 모두 사상 최고치를 경신했고, 이는 DASH가 선택권, 품질, 경제성 측면에서 달성한 성과에 따른 것이다. I answered the question to Mike, I talked about the fact that the cohorts continue to remain very strong. If I look at users, users are still growing at a double-digit rate. Users hit an all-time high in the quarter. Order frequency continues to be at an all-time high. A lot of that is being driven by the underlying work we’ve done, whether it’s selection, quality or affordability. All this has set us up well, not just for the third quarter, but going forward as well.

외식 사업은 안정적인 성장 추이이며, 식료품, 해외 사업 모두 외식사업보다 빠르게 성장중이다. And from an output perspective, if you think about the various lines of business, the restaurant business, the growth has actually been very stable for the last few quarters. Both grocery new verticals, international they’re growing much faster than the restaurant business as well as they have gained share across grocery as well as most of the international markets that we’ve operated in.

평균 주문액은 식료품 분야 성장이 크게 기여했다. 하지만 DASH가 가장 중요하게 생각하는 것은 이용자수와 이용 카테고리의 다양성이 증가하는 것이며, 매 분기 지속적으로 성장하고 있다. And to your second point around the overall AOV increase, we’ve seen some increase in the overall grocery business. Again, I wouldn’t think of that as a major shift. Our goal is to ensure that we are bringing the highest number of consumers to order from more categories and the consumers ordering for more categories, that number continues to increase every single quarter.

Andrew Boone(JMP) : GPM 증가 배경, 해외 확장 계획

GPM 서프라이즈가 나온 배경은? Thanks so much for taking my questions. Ravi, I wanted to ask about the gross profit margin outperformance in the quarter. I understood the call out on the insurance benefit, but is there anything else that you guys want to highlight in terms of the outperformance there?

Wolt가 유럽의 Tazz를 인수했는데 앞으로 어떤 국가의 어떤 기업들을 인수할 계획인지? And then Wolt acquired Tazz in Europe. Tony, can you just step back and talk about what may be attractive in terms of M&A targets going forward, and why that specific country and acquisition? Thanks so much.

CFO : 물류비 효율성 개선, 재투자, 광고, 규제비용이 감소한 결과이나 특정 GPM 수준을 목표로 하지 않고 장기 이익 극대화를 추구

연초 예상보다 DASH 팀이 잘 해냈으며 효율성 증가, 재투자로 인해 가능했다. Yes, Andrew. I’ll take the first one on the gross profit. Let me give you two ways to think about this. If you think of the business as a collection of businesses, what you’re seeing is, I mean, we performed really well. The team has executed really well compared to the plan that we have set for ourselves at the beginning of the year. We’ve driven efficiencies in some parts of the business. We’ve reinvested that in other parts of the business, and the output is what you’re seeing on part of the face of the P&L.

광고가 GPM 증가에 크게 기여했다. 또한 규제비용이 지속 감소하고 있다. 그리고 물류비 효율성도 개선되고 있다. 하지만 DASH는 특정 GPM을 목표로 사업을 운영하고 있지 않다. More specifically, if you think about the drivers, advertising has obviously been a driver in terms of gross margin improvement. The second thing I would call out, Andrew, is we’ve talked about the fact that regulatory costs will continue to reduce as we go through the year. That’s been another driver. And the last one is efficiency from an overall logistics perspective. But the key thing that I would underscore is — remember, I mean, we are not operating the business towards a specific gross margin percentage.

DASH는 장기적 관점에서 이익을 극대화하려고 한다. 이를 위해 모든 분야에서 효율성을 높여 이를 재투자할 것이다. What we’re trying to do is maximize overall profit dollars over the long-term. And the way we do that is every dollar of efficiency we find, we’re going to reimburse that back in the business. And our goal is to flexibly invest that up and down the P&L, wherever we see the opportunity. Our goal has always been to build a large business while continuing to be manically focused on unit economics. That’s how we’ve operated, and that’s going to be the same philosophy in which we operate the business going forward as well.

CEO : 지역/상품 확장, DASH 사업과의 보완성, 시너지 등 고려

인수할 때 이 회사가 새로운 지역으로 확장하는데 도움을 주는지, 이용자수나 상품 구성을 성장시킬 것인지, DASH가 스스로 성장하기 어려운 분야에서 성장을 가져다줄 수 있을지 고려한다. Hey Andrew, it’s Tony. On the second question with regards to international M&A. Our standards and VAR continue to remain really high and we are consistent in our approach, which really first and foremost, starts with asking ourselves the question, does this candidate help us launch a new geography, grow our TAM and/or our product portfolio. The second question we ask is, does this help accelerate us in a differentiated way that we couldn’t do ourselves organically.

장기적인 현금 흐름과 DASH의 경영 인력으로 해당 기업의 기회를 잡을 수 있는지도 중요하다. Three is, do we believe that by partnering with the candidate that we can achieve long-term cash flows. And the last one, perhaps the most important is do we have a team that has the management talent and bandwidth to execute on the opportunity in a single-threaded way. And when I look at that last one in particular, I mean, Wolt [ph] has been on an incredible run. I mean, ever since well, ever since founding, I mean, actually, I should say that it’s now been 10 years for Wolt, actually celebrated 10 years earlier this month, and they’ve achieved over $15 billion of sales for merchants in their lifetime and $3 billion of earnings for years, and they’ve just don’t rate in their geographies, and they continue to take share virtually everywhere they operate in and they’ve continued to help us perform just as a management team.

지난 3년 동안 Wolt는 확장을 지속할 수 있었으며, TAS와 협업할 루마니아 시장도 기대된다. And so when I look at the performance over the last three years, they certainly have earned the privilege to continue expansion. And then when I piece that together with TAS, playing in an attractive market in Romania, we get really excited about what the combination can provide.

James Lee(Mizuho Securities) : DashMart 현황, 유럽 퀵커머스(15분~1시간 만에 즉시배송) 시장 평가

DashMart가 잘 하고 있는 분야와 개선중인 분야, 성장 제약요인은? 유럽 경쟁사들이 퀵커머스에서 수익성을 확보하고 있는데 유럽 시장의 특수성은? Great. Thanks for taking my questions. Tony, I was wondering if you can comment about DashMart. And maybe can you give us an update like which business models are working and which business model is still working progress? And maybe talk about some of the growth constraints that we should be thinking about? So — and lastly, it seems like some of the European peers are able to make quick Commerce profitable. Maybe help us understand any differences you’re seeing between North America and Europe. Thanks.

CEO : DashMart는 빠른 재료 조달, 소매업체 유통 사각지대 보완

DashMart는 상인들이 빠르게 재료를 조달할 수 있도록 돕기 위해 만든 것이다. Sure. On DashMart, we’re very excited about how they progressed. I mean if I rewind the clock when we started DashMart 3, 3.5 years ago, mean the first push was making sure that we can actually be a national service. And one of the reasons for that was really in search of to help merchants actually because we’ve always viewed DashMarts over time as an infrastructure in which we can offer retailers to forward deploy their inventory. But first, we needed to prove to ourselves and then certainly to merchants, that we knew how to run these warehouses.

3년반이 지난 현재 DASH는 좋은 가격에 재고를 정확히, 빠르게 판매하여 그 목표를 달성했다. And I would say after 3, 3.5 years, the team certainly has achieved that marker. And so that or on their own have done really well in terms of learning how to execute by selling inventory exactly what’s on the shelf, which is very differentiated from a selling inventory that’s available in third-party stores. They’ve done it at great prices, and they’ve done it with awesome selection and very high reliability and speed.

DashMart는 스스로 점유율을 확대하며 성장하고 있다. 또한 다수 소매업체들과 파트너십을 통해 휴무 시간, 침투하지 못한 지역까지 사업을 할 수 있도록 인프라를 제공하고 있다. And so I think on its own, DashMart have just continued to grow, take share and do really, really well. But that was where DashMarts would end per se. I mean we’ve also seen quite a lot of progress in terms of our partnership discussions with a lot of retailers. So we’ve first started that in Canada and partnering with Loblaws, but we’ve also now have started some of those journeys here in the U.S. as well as in other countries, where we are providing that infrastructure on behalf of retailers so that they can gain additional business at hours that they usually are closed in as well as in geographies that they may not be as penetrated in.

결국 DashMart는 스스로의 성장 뿐만 아니라 소매업체들과 파트너십 측면에서 잠재력이 높다. So — we’re quite excited about the potential that DashMarts bring both individually, but more so as in partnership with retailers and merchants — and that’s kind of what I expect going forward.

Mark Mahaney(Evercore) : 신제품 피드백, 도시/교외 이용자 차이

24.9월 출시 신제품에 대한 판매자 피드백은? 도시와 교외 DashPass 집중도에 차이가 있는지? Hey, this is David for Mark. A question on the commerce platform. Do you have any early feedback from merchant customers around the new products that you released last month? And then one more on the Lyft partnership, could you talk about the concentration of DashPass members between urban and suburban markets?

CEO : 지역경제 성장, 디지털 전환 촉진을 통한 큰 시장 내러티브가 중요, 특정 집단을 타게팅하지는 않음

DASH는 1. 지역 경제를 성장시키면서 2. 지역 경제의 디지털 비즈니스 전환을 지원하고 있다. 결국 DASH를 활용하여 상점들은 디지털 역량이 강해지고 있다. Sure. On the first question with regards to The DoorDash Commerce platform. I mean this announcement for us really, I would say, has been a few years coming, meaning that it really just encapsulates what DoorDash has now become, which is really two parts, right? Part one of our mission has always been to grow the local economy, and we do that by bringing incremental sales with the wrap. And the second part is to empower local economy to become digital businesses. And so a lot of these physical businesses now are using products like DoorDash Drive or storefronts or some of the other products that we’ve talked about in order to become digital powerhouses in their own rights and with their own customers.

DASH 플랫폼에 몇십만 사업자가 입점하여 소비자와 판매자가 연결되고 있어 디지털 역량을 강화하려는 업체들의 입점을 유인하고 있다. And so — we are seeing that. I mean when you have hundreds of thousands of businesses now who are part of the DoorDash Commerce platform. So I think the numbers speak for themselves in terms of the excitement. And I guess, from their perspective, if you look at DoorDash, the marketplace as the leading local commerce marketplace, where we do the best job of building products that connect consumers to merchants why wouldn’t you want to partner with that and have that for yourself as the retailer that’s trying to become more and more digitally native. And so that’s what we’re seeing.

DASH는 특정 이용자 집단을 타게팅하려 하지 않고, 가장 유용한 제품을 만들어 가입자수를 늘리는데 집중하고 있다. With respect to — I think your second question about DashPass, I mean we see strength and opportunity in terms of any partnership, whether it’s Lyft or Chase or MAX across all of our members. Otherwise, we wouldn’t be that excited if it was just trying to target one group of customers while excluding a different group of customers. But again, I think it’s important to just understand what the main thing is, 80% of what I believe is important for building membership programs is by building the most useful products, which get used the most often.

다만 Lyft와의 협업은 DASH를 지역적으로 확장하는데 도움을 줄 것이라고 생각한다. That’s actually how you earn the right to even start a membership program. So that’s the 80%. And then the 20 for us is in partnerships, and we’re super excited about the Lyft partnership as we are about our other partners, and we believe that they’ll help us in any geography.

CFO : 구독자수 1,800만명, 어디에나 존재

DashPass는 지역 상권을 선도하는 구독 사업이며, 성장하고 있다. 3Q 구독자수는 1,800만명을 넘겨 사상 최대치이며, 그들은 도시나 교외나 모든 곳에 있다. And David, just to add to that, right. Like we don’t — I mean if you think about DashPass, itself, it’s a leading local commerce subscription program, and we continue to grow. In fact, in the third quarter result, we hit a record number of subscribers, which was an all-time high, over 18 million plus DashPass members. They’re everywhere, right? They are not differentiating between urban or suburban. We see strength across the board, which you see in the overall share gains that we’ve had in the quarter as well.

Michael McGovern(Bank of America) : 자율주행, 광고효과

자율주행 활용 계획이 있는지? 파트너십 전략에 포함되는지? 식당 상위노출시 소비자 전환에서 어떤 효과가 있으며, 광고에 미치는 영향은 무엇인지? Hey guys, thanks for taking my questions. I have two — there’s been a lot of attention on the topic of AVs recently, obviously, for rideshare, but do you have a view on the potential future of the delivery use case for autonomous vehicles? Is that something that you may be looking into for your partnership strategy? And then secondly, on restaurant sponsored listings, what are the latest trends that you’re seeing in terms of merchant ROACE [ph] and consumer conversion? And how is that playing out in terms of demand for the ads? Thank you.

CEO : 자율주행은 Last Mile Delivery 연구중, 시장 성장에 따라 광고효과는 매우 큰 상황

DASH는 17년부터 자율주행에 대해 연구해왔다. Mike, I can take both of those. On the first question related to autonomy. I mean, we’re very excited. I think it’s been in some ways, as someone who’s been working in the autonomous space now for several years. It’s a long time coming. I think some of the developments that maybe you’ve been reading about or seeing — so maybe that’s where I’ll start which say that we’ve been working on the autonomy delivery problem for several years now dating as far back as 2017.

다만, 마지막 10 피트(Last Mile Delivery) 배송이 상당히 까다롭다 And I think the most important thing to tell you about it after working on it for a while now is that it’s actually quite different from autonomous right halo. And it’s probably obvious to states. But when you don’t have a passenger who can just easily go in and come out of the vehicle, and you have to actually load and unload the vehicle when it comes to item delivery, that last 10 feet is actually quite tricky.

DoorDash 초기 사람들은 우버와 비슷한 서비스라고 생각했었다. And so it reminds me a lot of actually how DoorDash got started. I think when DoorDash got started 11 years ago, a lot of people thought, oh, you should — this is delivery and something like ride hailing might be similar when it comes to dispatch algorithms or something like that. But if you were to apply the same dispatch algorithm for ride hailing as you did for delivery, you’d almost always make the wrong decision.

하지만 우버와 달리 배달은 음식이 준비되지 않거나 재고가 준비되지 않으면 모두의 시간이 낭비된다. 이 점이 자율주행 택시와 배달에서도 큰 차이라 생각한다. 따라서 DASH는 원칙으로 돌아가 자율주행 기술을 도입하는 것보다 기술을 통해 이 시스템이 잘 작동하도록 만드는 것을 우선시하고 있다. If you dispatch the closest driver to a passenger, for example, which is what you would do in ride hailing and you apply that to delivery and either the inventory is not available or the food is not ready, then you kind of wasted everyone’s time. And I would say that they are very fundamental differences in a similar way for autonomous delivery versus autonomous ride hailing. And so we’re taking a first principles approach in terms of what we’re building at DoorDash and in terms of marrying technology as well as operations to build a system to make this work.

DASH는 잠재적 파트너와 협의를 많이 하고 있지만 자율주행에 대해 알려진 바와 현실은 매우 다르다. We’re pretty excited about what we’re working on as well as conversations with potential partners as well. But it’s a very different problem from maybe some of the things that you’ve read and but we’ll have hopefully some things to share in the future, and we’ll tell you more about it then.

시장이 규모를 고려할 때 빠르게 성장하고 있다는 점을 고려할 때 광고효과가 크다. The second question was around, I think, just adds and just trends in that business. I think more and more of what you’re saying is that you just see kind of a continued progress on that business. And I think it starts from the fact that our marketplace continues to grow at pretty high rates, given its scale.

광고 성장은 시장 성장보다 먼저 온다. 식당의 광고지출에 따른 수익률은 점점 높아지고, 소비자 전환율도 개선되고 있다. 이것이 큰 시장과 결합되면 광고 비즈니스는 빠르게 성장할 것이다. And I’ve always said that a successful ads business is preceded and always preceded by a successful marketplace business. And so that’s what we continue to see where our ads business continues to have leading ROACE or return on ad spend for advertisers for restaurants and increasingly for retailers. And we see our consumer conversion improving as well where they’re approaching organic rates. And so I think the combination of these two things in tandem with a marketplace that is the largest for what it does in terms of connecting consumers locally to merchants, that’s why you’re seeing some of the results in terms of the ads business continuing to grow at very high rates at high scale.

Lee Horowitz(Deutsche Bank) : 식료품 광고 수요

식료품 부문에서 급성장하여 시장이 커지고 있으며, 이는 식료품 파트너들의 광고에 대한 관심을 불러일으킬 것이다. 내년도 광고 예산 집행을 고려하면서 DASH에 관심을 표시한 적 있나? Hi, thanks. Maybe sticking with ads and moving over to CPG advertising. You guys have obviously been stacking multiple quarters of really strong grocery volume growth and getting that marketplace to scale. I guess this is probably presumably grabbing the attention of your CPG advertising partners. Have you gotten any indication from those partners in your conversations as they think about budgets for next year, that they be leaning a bit more aggressively into your platform, just given how much you have grown over the last year or so?

CEO : 성장성, 가맹 식당 매출, 정보, 상품 구성 측면에서 관심

식료품점들은 배달 분야에서 증명한 성장성 뿐만 아니라 가맹점에 식료품을 팔 수 있다는 점, 지역 상권에 대한 가장 많은 정보를 보유하고 있다는 점 때문에도 관심을 많이 보이고 있다. Yes, I can follow on to the answer to the last question here. I mean the short answer is yes. I mean I think CPG advertisers have always been really excited about us because not only because of our strength in growth outside of restaurants, but also just the combined view that we can offer because you can certainly sell a CPG item across both restaurants and retailers across multiple categories. And by being the largest local commerce player, we get to offer the most data and most views and most shots on goal for every brand to win their fair share. And I think that’s what’s increasing the excitement.

DASH는 상품 포트폴리오를 구성하고 성숙시키는데 능숙하며, 식료품 기업들도 이를 중요하게 생각할 것이다. On the flip side, I think the team, our team also deserves quite a lot of credit for building and maturing the product portfolio, which is still an area of emphasis for both our CPG ad partners as well as our restaurant partners.

Lee Horowitz(Deutsche Bank) : 식료품 경쟁사 대비 강점

수직적 통합을 이룬 자사 배송 파트너들도 존재하는 등 식료품 분야 경쟁이 심한데 DASH가 승자가 될 수 있는 이유는 무엇인지? Great. Thanks. And maybe one follow-up just on grocery competition holistically. Obviously, it’s very fierce. You have first-party delivery partners who can perhaps lean in on price, given vertical integration. You have other marketplaces that have other verticals that they can monetize on besides grocery and then obviously some focused grocery marketplaces. I guess within that hypercompetitive environment, where do you see as the most defensible sort of characteristics for DoorDash that should allow you guys to come out as one of the key winners in this vertical over a longer period of time.

CEO : 제품 경쟁력 강점을 토대로 이용자 유지, 주문빈도 성장중

최고의 제품을 만드는 것이 DASH가 경쟁에서 이기기 위한 방법이다. 11년전 시작된 미국 배달 시장, 현재의 해외 시장 모두 최고의 제품을 제공하는 것으로부터 이용자와 배송빈도 유지가 시작되었다. Well, it starts with building the best product. I mean — and I think this is kind of how you get out of any competitive market. I mean if you look at the restaurant delivery industry, that’s how it started 11 years ago, too. And I think that the way that DoorDash has come to its current position in restaurant delivery, whether it’s in the U.S. or whether you look at us outside the U.S. or Wolt outside of the U.S. It starts by building the product that achieves the highest retention and order frequency, which was — which is really a testament that you built the best product. And it allows you to most efficiently grow. So I think, first and foremost, it comes down to product execution.

현재 DASH가 식료품 배달 분야에서도 선두기업으로, 고객의 절반 이상이 식당 외 배달을 주문하고 있다. And I think you’re seeing that. I mean you’re seeing that where we are now the first place that consumers come to grocery delivery for, if they are a new customer to grocery delivery, that’s also true if you’re just getting something delivered locally outside of restaurants. And so we’re seeing that — it’s always been true for us in restaurants or for several years now, it’s been true where over half of customers that are shopping for restaurant delivery first comes to us for deliveries now outside of restaurants.

DASH는 이용자 유지, 주문빈도 측면에서 강점을 보이고 있으며, 이는 선택권, 품질, 가격, 서비스 개선에 따른 것이다. 이러한 경영상 우선순위에 따라 높은 성장 속도가 유지되고 있다. It’s approaching that market, too. And so we’re seeing that. We’re seeing strength on the retention and frequency side with every single cohort that continues to increase as we improve our selection, improve our pricing, improve our quality of delivery, improve our service. And I think that the maniacal focus is what allows you to build the compounding advantage over time and allows you to grow at higher rates over multiple years.

CFO : 가맹점들도 DoorDash 기여도 인정

가맹점들도 DoorDash가 매장 매출 성장을 늘리고 있다고 피드백을 주고 있다. And Lee, just to add to that, right, just on the consumer side, but we get good feedback from the merchant side as well, where merchants that we partner with have said that we’re driving incremental same-store sales growth for them. The quality that we drive to the merchant has also been great. And you see that in the results where, A, we are the fastest growing in the U.S. as well as gaining share. And also from a cohort perspective, right, the retention and order frequency continues to increase.

CEO : 플랫폼 이용자가 많아 높은 광고효과

DASH는 음식 배달 분야 선두기업으로 식료품과 같은 다른 카테고리 광고주들에게 큰 도움이 된다. Yes. I think the final thing I believe Lee is that like we also just get the most shots on goal. When you think about what gets delivered most often, it’s prepared meals, which is in a different way of saying restaurant delivery. And because we’re the leading player in that space and because we’re also both in terms of size as well as the frequency we just get more at [indiscernible] with these customers, which is very helpful, especially if you’re not in the restaurant category, say, in grocery or other retail categories. And it’s also really helpful for advertisers, too.

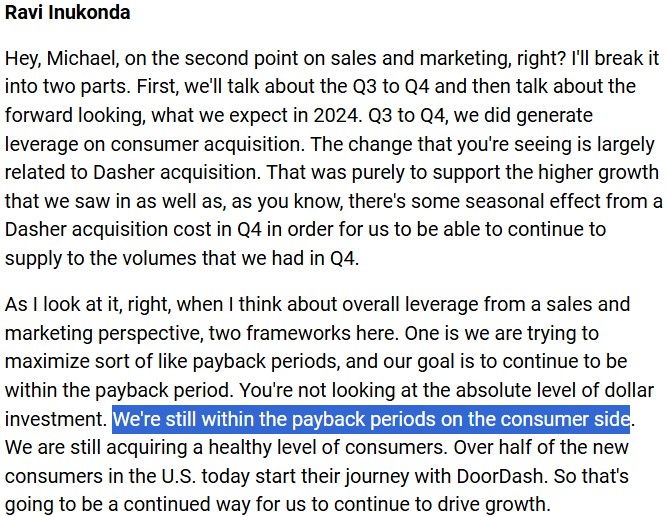

John Colantuoni(Jefferies) : Dasher 보상, 주문 확대를 위한 투자 방향

Dasher 인센티브는 어떻게 변하고 있는지? Great, thanks for squeezing me in here. So I want to start with sales and marketing leverage continues to be a really nice tailwind for EBITDA. Can you peel back the onion and talk a little bit about contribution from driver incentives. And sort of when you think about beyond the near term and look at supply and demand dynamics and your investments in driver experience, how are you thinking about the magnitude of the ongoing contribution to margin expansion from leverage on incentives?

주문량을 늘리기 위해 어떤 방향으로 투자할 것인지? And second question, just turning to grocery. How important is capturing more of that big basket weekly shop to your long-term profit aspirations in grocery? And what are the capabilities and investments you still need to make to start driving more of those large basket orders? Thanks.

CFO : 제품 개선이 최우선

모든 영업과 마케팅은 제품에서 시작된다. Yes, John, I’ll start, Tony will be back. On your point around sales and marketing, I mean, look, John, when I think about sales and marketing or any type of operational efficiency that we drive in the business, it always starts with product because ultimately, product drives retention for us, which drives leverage in sales and marketing. If you break that apart, we’ve seen a lot of leverage on Dasher acquisition over the last couple of years.

제품이 개선되면 Dasher가 배달을 더 용이하게 할 수 있고, 더 오래 유지되어 영업 레버리지를 높이게 된다. 또한 이용자 측면에서도 최적화가 잘 이뤄졌기 때문에 레버리지가 발생되고 있다. A lot of that is being driven by the product improvements that we’ve made. It’s easier for Dashers to onboard. It’s easier for Dashers to get paid, all of that is driving retention of existing Dashers higher, which ultimately drives leverage from a sales and marketing perspective. The second thing I would say is even on the consumer side, the teams have done a pretty good job of optimizing at a channel level. So you’re seeing leverage from a consumer acquisition cost perspective as well.

DASH는 제품을 계속 개선하여 영향력을 높일 것이나 변화의 속도는 조금 느려질 수 있다. 다만 Dasher 인수, 소비자 확보 여부를 고려할 때 레버리지를 높일 기회는 충분하다. Looking ahead, I mean, I do expect us to continue to improve the product, which ultimately will drive leverage on sales and marketing. But I expect the pace of change to be slightly slower than what we saw in the last couple of years. But overall, when I think about whether it’s Dasher acquisition or consumer acquisition, there’s still opportunity for us to continue to go and drive leverage there.

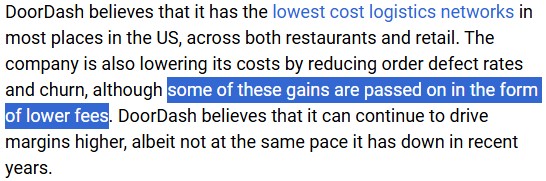

CEO : 배송비가 가장 낮은 수준이어서 배송이 작아도 지속가능

DASH는 배송, 물류 관련해서 경쟁사 대비 가장 낮은 비용 구조를 갖고 있다. And John, on the second question with regards to just larger baskets and grocery. I mean, I would all of that for us is really just cherries on top of the cake, meaning that we don’t actually need large baskets to make the math work for grocery. And that’s because we have the lowest cost structure when it comes to delivery and logistics.

DASH는 이용자, 식료품점 모두에게 작은 배송도 효율적으로 할 수 있음을 보여주었다. And so one of the things that we’ve been able to do is actually build a very high-growth business with these smaller baskets as a way to introduce ourselves to consumers and grocers alike. And I think it’s actually surprised us just how large that market is. I think in some ways, it resembles almost what happens in Europe, where people instead of buying one large basket for the week, they might buy several smaller baskets for the week. I think that’s a phenomenon that we can afford that others may not be able to.

고객들이 몇 번 구매한 이후 후속 주문들에서는 배송 규모가 커지고 있는데, 규모가 커지지 않더라도 지속가능성은 확보되어 있다. I think — so anything that we get, and we are getting these larger baskets, especially after customers buy with us a couple of times they start mirroring kind of their habits, where they will buy maybe a couple of smaller baskets during the week and by one large basket on the weekend. So we are seeing that. And we see that with every single subsequent order. We also see that with every subsequent cohort. But it doesn’t have to be a focus for us to make the business financially sustainable.

CFO : 배달 사업에서 이용자, Dasher가 확보되어 수익 기회에 온전히 집중

DASH는 모든 카테고리의 사업을 구축하려고 하고 있으며 플랫폼에 소비자가 이미 있기 때문에 전략적으로 이점이 있다. John, just to add to that, right, I wouldn’t think of it as a large basket versus a small basket. For us, when we build the business, we’re trying to build the business for all baskets. If you think about it going back to your sales and marketing question, we have a strategic advantage because remember, we already have consumers on the platform.

또한 플랫폼에 Dasher들도 있다. 따라서 (고정비 지출이 필요없기 때문에) 수익성이 높다. 따라서 작은 배송도 수익성을 확보할 수 있으며 수익 기회가 있는지에 온전히 집중할 수 있었다. We already have Dashers on the platform. So the flow-through from a gross margin to contribution margin for us is very high. When I think about the unit economics, team has done a phenomenal amount of work over the course of the last year. When I look at that in the P&L, that doesn’t concern me. We have a combination of us being able to make the math work at smaller baskets, plus the sales and marketing leverage where we are focused on is what’s the size of the opportunity in terms of scale as well as overall gross profit dollars.

DoorDash 결론 : 자본배치, 성장성, 수익성이 고밸류 만회

(성장성) 소비자, 구독자, 총주문액, 평균주문액 등 지표가 YoY 20% 내외로 성장하고 있으며, 내러티브 측면에서는 해외 시장에서 미국 시장과 유사한 성장 경로를 밟아가고 있고, 식료품 등 다른 카테고리로의 확장도 성공적이다.

(수익성) 질적으로는 이용자수/구독자수를 바탕으로 광고 매출이 확대되면서 수익성이 개선, 네트워크 효과, 규모의 경제가 향후 수익성 개선 논리로, 신규 시장 적자도 상쇄하고 전사적 흑자

(자본배치) ‘소비자에게 제공되는 상품의 품질’이라는 핵심가치를 우선시하여 협업, 인수를 통해 카테고리 확장, 지역 확장을 이뤄나가는 자본배치 방향성이 현재까지 수익성 개선을 견인

(밸류에이션) 현 시총은 $646억(약 87조원)으로 24.3Q $1.62억(약 2,187억원)을 4배(실적 개선추이이므로 보수적 전망이다)했을 때 PER은 100 정도이다. 하지만 네트워크 효과, 규모의 경제 등 강한 경제적 해자의 근거, 성장 내러티브와 매출 성장, 이익 개선 추이를 감안하면 섣불리 고평가로 보기는 어렵다.

가치투자 커뮤니티를 성장시켜나가고 있습니다. 운영 계획과 방향성을 한 번 읽어보시고, 텔레그램을 소통채널로 활용하고 있으니 공감이 가신다면 참여해주세요! 쌍방향 소통을 원하는 분들은 카카오톡 채널로 와 주시면 좋을 거 같습니다. 연말까지 투자 아이디어 대회도 진행하고 있으니 많은 참여 부탁드립니다.

전미 외식협회와 Fortune Business Insights에 따르면, 증가하는 가처분소득, 여성 경제활동 참가율 증가, 바쁜 생활 패턴, 패스트푸드의 편의성, 안정적인 노동시장 등은 배달 시장 수요를 증가시키는 메가트렌드들이다.

소비자 편의성

세계적인 COVID 유행 이후 사람들은 음식을 배달받는 ‘맛’을 알아버렸고, 쇼핑하거나 외식하는 데 시간을 들이지 않고 식사하는 데 익숙해져버렸다. 소비자 편의성을 증진시켜주는 변화는 되돌리기 힘들고, 지속성이 높다.

침투율

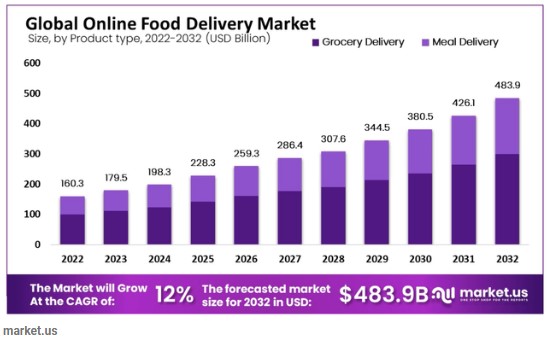

온라인 음식 배달시장은 2030년이 되어도 전체 미국 음식 시장의 10% 정도를 차지할 것으로 예상된다.

또한, DASH가 전체 미국 음식 시장의 한 자릿수 점유율만 차지하고 있는 현 시점에는 충분한 성장의 룸이 남아 있다.

또한 식료품 분야도 다른 분야 대비하여 총 시장 대비 전자상거래 비중이 12%로 낮다.

성장률 추정치

이에 따라 전 세계 음식 배달 시장은 ’22~’32년 10년간 CAGR 12%가 기대된다. (어떤 기준으로 봐도 10년 평균 CAGR 12%는 주가가 10배 이상 올라가는데 충분한 속도다)

DASH는 영위하고 있는 산업을 미국 내 음식 배달에 국한하지 않고, 전 세계, 생활용품 LMD 사업 전체를 장악하려는 ‘큰 내러티브’를 그리고 있다. 모든 카테고리의 LMD에 대한 구체적인 자료는 없지만, 음식 배달 분야와 비교해서 확연히 느릴 이유는 없는 것으로 판단된다.

전망에 영향을 줄 수 있는 중요한 요인은 ‘자율주행 로봇’의 활용이다. 최근 자율주행 로봇을 LMD에 활용하려는 연구가 활발하며, DASH도 Wing社와 협업하여 22년 호주 퀸즐랜드에서 드론 배달을 시범운영했고, 24년에는 버지니아에서 첫 배달을 한 이후 호주, 미국, 캐나다에서 35만건을 배달했다.

자율주행은 DoorDash의 비용을 낮춰주지만 새로운 경쟁요인이 될 수 있다는 점에서 그 영향을 장기적인 관점에서 모니터링해야 할 것이다.

점유율

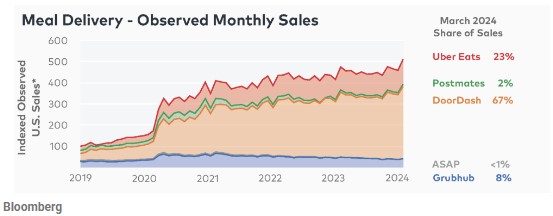

DASH의 미국 배달시장 점유율은 67%로 2위 경쟁자 UberEats 대비하여 압도적인 상황이다.

특히, 매분기 시장을 상회하는 매출 성장을 시현하면서 경쟁자들의 점유율을 가져오고 있다.

식료품 시장은 음식 배달시장보다 더 큰 시장인데, InstaCart가 1위 사업자로 소형 배달 시장의 50%, 대형 배달 시장의 70%를 차지하고 있다.

다만, 식료품 시장에서도 앱 사용자 트래픽을 바탕으로 3분기 연속 100%를 상회하는 속도로 빠르게 매출을 성장시키고 있어서 점유율 확대가 기대된다.

점유율을 확대시키는 경제적 해자에 대해서는 후술하도록 하겠다.

이익률이 증가하는가?

DASH는 현재 흑자전환을 하지 못한 상태로, 이익을 논하기 어려운 상황이다. 다만, 유통 산업이 그렇듯이 점유율을 확보하기까지는 경쟁사와 치열한 점유율 싸움을 할 수밖에 없고, 그 과정 속에서 최대한 싼 가격에 좋은 경험을 제공하여 ‘지배적 사업자’ 지위를 공고히 하는 것이 중요하다.

DASH는 이러한 관점에서 시장 확장과 기술개발(자율주행, 드론 등), 요금 인하 등을 통해 이익을 제한하고 매출을 극대화하는 전략을 사용하고 있다.

이는 아마존이 커지는 전자상거래 시장에서 높은 R&D 투자 비중과 낮은 이익률을 상당기간 유지한 전략과 일치한다.

결국, 이익률을 희생하여 매출 극대화 전략을 사용하고 있는 것은 DASH의 사업 구조와 전략상 불가피한 선택으로, 다른 강점을 통해 상쇄되어야 할 약점으로 보인다.

다만, 광고 부문 매출 성장, 구독자 매출 증가로 인해 이익률이 성장하고 있으며, 24.2Q 이익률 저하는 소송비용, 사무실 관리비 등 일회성 비용 영향임을 감안해야 한다.

DASH는 현재 적자를 내고 있다는 것만으로 폄하하기에는 전략적 방향성이 명확하며, 시너지가 명확한 사업들에 자본을 투입하여 성장 역량을 확보하고 있다.

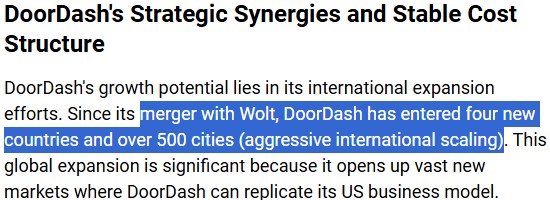

대표적인 인수합병이 Wolt라는 핀란드 기업으로, 유럽에서 DASH와 유사한 사업을 진행하던 기업이었다. 인수합병을 통해 DoorDash는 4개국, 500개의 도시에 사업을 새로 확장할 수 있었다.

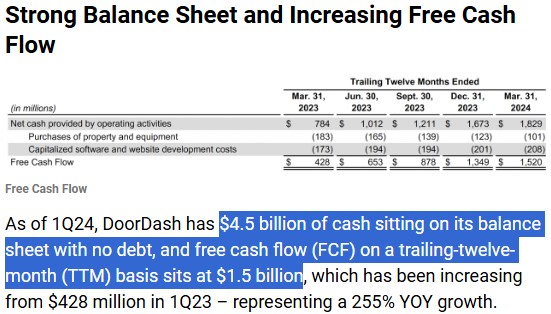

또한, DASH는 적자기업임에도 부채가 없고 $45억의 현금을 보유하고 있고, 현금흐름이 충분하여 유동성 리스크가 없고 필요할 때 인수 여력이 충분한 기업이다.

이러한 점을 고려할 때, 위험을 충분히 회피하면서 자본을 효율적으로 배치해 왔으며, 전략적 시너지를 고려한 인수합병이 원활히 이뤄져 왔다고 평가할 수 있겠다.

결론 : 나의 실수를 성장이 커버해주는 기업

DASH는 점유율 확대, 영역 확대, 국가 확장에 따라 내러티브가 명확하며, 네트워크 효과, 규모의 경제에 따른 경제적 해자를 보유하고 있고, 적자 기업임에도 부채를 사용하지 않고 시너지 있는 사업을 인수할 여력을 보유하고 있어 자본배치를 잘 하고 있는 기업으로 평가할 수 있다.

다만, 한 가지 약점은 적자 기업으로, 아직 수익성을 증명하지 못했다는 것이다.

하지만, 이러한 적자가 회사의 전략적 선택의 결과라는 점을 이해한다면, 현재 주가가 고평가 되었더라도 지속되는 성장에 따라 지금의 주가가 높지 않았음을 시간이 증명해줄 거라고 생각한다. (성장주에 투자하면 나의 실수가 성장으로 커버된다는 것은 이 글을 참고)

진정한 가치투자자들을 동료로 모집하고 있습니다. 모집글을 읽어보시고 공감이 가신다면 텔레그램 채널을 플랫폼으로 활용하고 있으니 참여해주시면 감사하겠습니다!